-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Maple Leaf Education Limited (1317.HK) - Fair annual results along with larger policy risks

Thursday, December 13, 2018  8691

8691

China Maple Leaf Education Limited(1317)

| Recommendation | Neutral |

| Price on Recommendation Date | $3.350 |

| Target Price | $3.380 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

China Maple Leaf Education Systems Limited is a leading international school operator, from preschool to grade 12 education (K-12) in China. In view of the recent policies, we believe the business risks in compulsory education and kindergarten will be very large. As a result, we downgrade Maple Leaf from “Accumulate” to “Neutral”, with a target price of HK$ 3.38, 0.8% potential upside. (Closing price at 7 December 2018)

Annual Results Update

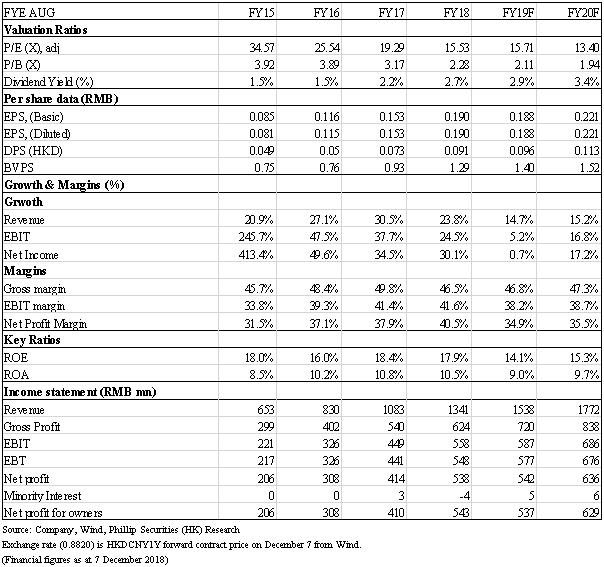

The revenue of Maple Leaf was RMB 1.34 billion, up 23.8% YoY, but 7.7% lower than our estimate, where it is because the average tuition fee per student and the additional service revenue were lower-than-expected. In the period, the proportion to tuition fees revenue of high schools, middle schools, elementary schools, preschool and foreign national schools were 48%, 17%, 28%, 5% and 2% respectively. The average school enrollments in 2018 was 29,783, rose by 31.1% YoY, in line with our estimate. By the end of September, the Group was operating 92 schools, which are 14 high schools, 23 middle schools, 24 elementary schools, 28 preschools, and 3 foregin national schools. In addtion, the gross profit margin dropped from 49.8% to 46.5%, due mainly to the surge in the cost of teaching staff, and it is also 3.5% lower than our estimate. However, Maple Leaf has done well in administrative cost control. The administrative expense as of revenue decreased from 14.3% to 11.6%, 2.4% lower than our estimate. Thus, the profit before tax was in line with our expectation, about RMB 548 million, while the net profit was RMB 538 million, 4.9% higher than our estimate.

Policy risks

On 10 Aug, Ministry of Justice of the PRC announced "中華人民共和國民辦教育促進法實施條例(修訂草案)(送審稿)", where the article 12 and 45 have the largest influence on the conpulsory education.

Article 12: The enterprise of education institute may not control non-profit private schools through mergers and acquisitions, franchise chain, agreement control, etc.

There are two key points in this article. First, it limits the business development in compulsory education. As the compulsory euducation must be non-profitable, it means compulsory education operators are not allowed to perform any mergers, acquisitions and Franchise. Second, as to the word “agreement control”, although it was not well-defined in this draft, it literally related to the VIE structure of the listed education companies. If the VIE structure is prohibited, the education institutes will not be able to distribute profits through related party transactions, where listed companies like Maple Leaf will be adversely affected.

However, there are some other interpretations in market, where they believe this article does not aim to ban the M&A, instead it prohibits a sponsor managing several schools. It hopes to reduce the risk in education operation by the practice of one sponsor one school. Besides, based on the article in "學前教育改革發展意見" promulgated on Nov 15 by State Council (Social capital shall not control kindergartens held by state-owned assets or collective assets or non-profit kindergartens through mergers and acquisitions, entrusted operations, franchise chains, use of variable interest entities, and agreement control), the word “variable interest entities” and “agreement control” are mentioned separately, implying that agreement control does not mean VIE structure.

But, we think those interpretations are too word-splitting. In fact, the keys of a policy are the stand and intention of the government. As early as 2016, when submitting the third trial of “民辦教育促進法修正案(草案)”, Zhu Zhiwen, deputy minister of education, has said: “Compulsory education reflects the will of the state, the basic public service that the government must provide, and the obligation that the state must enforce. Compulsory education determines its unsuitable for-profit private schools. Otherwise it may affect the implementation of compulsory education government responsibility, affect the balanced development of compulsory education, and even increase the burden on the people.” It clearly states the stand of government that compulsory education must be non-profitable. Asides that, on June 25, the Ministry of Education and other 13 departments announced the "民辦教育工作部際聯席會議2018年工作要點", which stated that it is necessary to monitor the behavior of private schools to prevent private schools from making profits in the name of non-profit. Therefore, we are more inclined to believe that the government is hoping to further regulate non-profit schools, thereby preventing private schools from making profits in the name of non-profit.

Article 45: Private schools shall disclose related party transactions. The Ministry of Education and Human resources and Social security shall strengthen the supervision of the signing of agreements between non-profit private schools and stakeholders, and the necessity, legitimacy and compliance of agreements involving major interests or long-term and repeated execution shall be conduct an audit review.

Although there has been regulation of related party transactions in the previous draft, there are further explanations for regulation in this edition. First, the information disclosure system for related party transactions has been extended from only non-profit private schools to all private schools. In addition, this article clearly states which government departments need to supervise related party transactions and conduct audits for their necessity, legitimacy and compliance. Among them, we think that the word “necessity” is relatively important because listed companies now transfer profits from schools in the name of various service companies, and the necessity of their transactions is doubtful. If the related party transactions are strictly regulated, the compulsory education business cannot distribute dividends to shareholders. As mentioned above, the government intends to prevent schools that are profit-making in the name of non-profits. We think this article in line with the government's position.

In addition, the State Council promulgated the "學前教育改革發展意見" on November 15 this year, in which Article 24 indicates that "the private kindergartens are not allowed to be listed by either alone or as part of assets. Listed companies may not invest in for-profit kindergartens through financing in stock market and is not allowed to purchase for-profit kindergarten assets by issuing shares or paying cash.” This will undoubtedly have a great impact on the listed companies that operate kindergartens. In the future, there is an opportunity to delist or spin off to the listed companies.

In view of this, we believe that Maple Leaf's compulsory education and kindergarten risks are very large, and then it may need to spin off to the corporate structure.

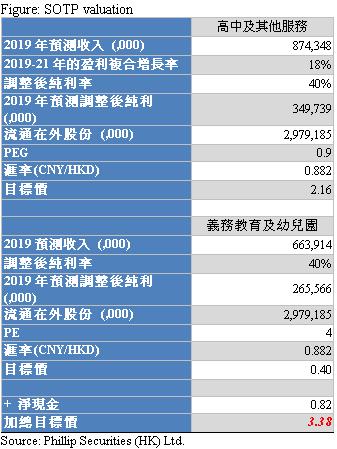

Valuation

As mentioned above, we believe that Maple Leaf's compulsory education and kindergarten risks are very high. It is very likely that the business will not be able to pay dividends to shareholders in the future. However, since it is generally believed that there will be five-year grace period, we assume that compulsory education and kindergarten business spin off five year later. We give 4x P/E ratio for the business to reflect its value before divestiture.

High school and additional service revenue will become the main source of revenue for Maple Leaf in the future. Although the management expressed their target to build a pyramid-like student structure in the annual result meeting, it will increase investment in kindergartens, elementary schools and middle schools, but we believe that if the policies of that kindergarten cannot be the asset of a listed company and elementary and middle schools must be non-profitable have been taken into effect, we expect the Group's high school and other additional service to remain strong, as the group can only develop its high school business. We only give 0.9x PEG (a 18% of CAGR on adjusted net profit in 2019-21F) to reflect the increase in the effective tax rate and the payment of land transfer fees after the high school segment turning into for-profit.

We derive a target price of HK$3.38, significantly 55.4% lower than the previous target price to reflect future policy risks; the rating has been downgraded from “accumulate” to “neutral” with a potential upside of 0.8%. (CNY/HKD = 0.882)

Risk

1. VIE structure prohibited in China

2. The grace period of policies is shorter than expected

3. New acquired schools were not able to add value

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()