-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CEB WATER (1857.HK) - Results of 3Q2019 in Line, M&A Projects Enhance Businesses

Friday, November 22, 2019  29042

29042

CEB WATER(1857)

| Recommendation | BUY |

| Price on Recommendation Date | $1.810 |

| Target Price | $2.660 |

Weekly Special - 3306 JNBY Design Limited

Company Update

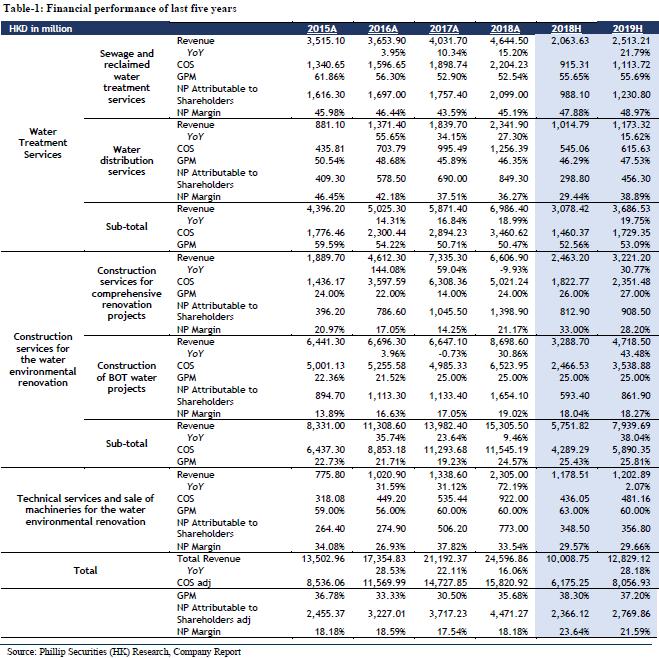

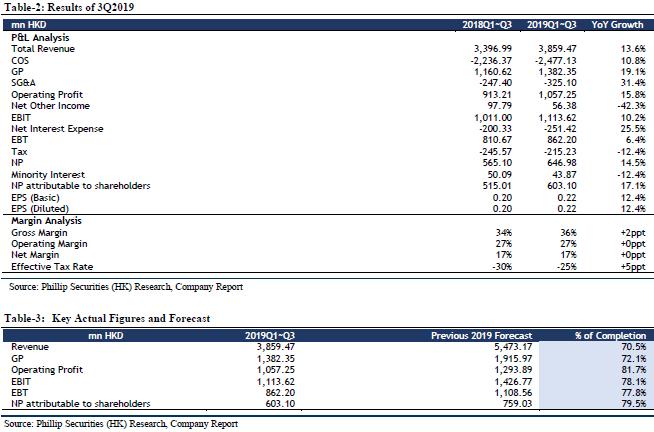

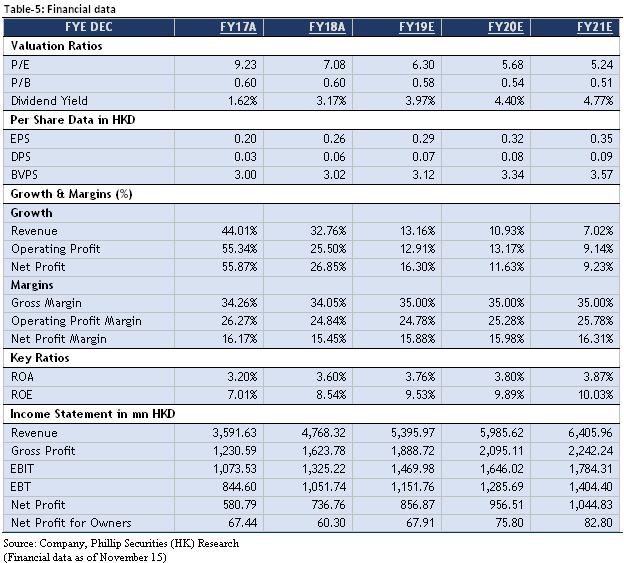

For the nine months ended 30 September 2019, the company's revenue was HKD 3.859 billion (corresponding period in 2018: HKD 3.397 billion), representing an increase of 13.61% YoY and 8.3 pts compared with 2019H; among which the revenue of 3QFY2019 was HKD 1.374 billion (corresponding period in 2018: HKD 1.037 billion), representing an increase of 33% YoY, which is slightly lower than our expectation; the increase was mainly attributable to the increase of HKD 193.07 million in construction revenue, HKD 85.85 million in operation revenue, HKD 23.20 million in finance income and HKD 35.47 million in other kind of revenue. The increase in construction revenue was mainly attributable to the construction of river-basin ecological restoration projects in addition to the expansion and upgrading of several waste water treatment plants. The increase in operation revenue was the result of the commencement of operation of new projects and the tariff hikes for several projects effected. The increase in finance income was due to the increase in contract assets.

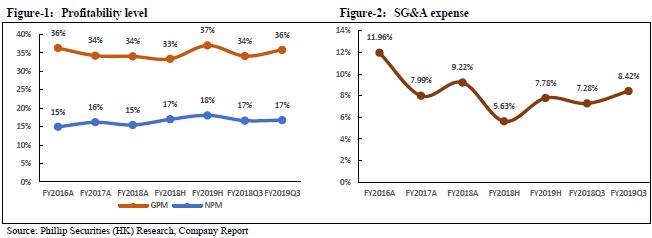

The gross profit was HKD 1.382 billion (corresponding period in 2018: HKD 1.161 billion), representing an increase of 19.1% YoY and 2.3 pts compared with 2019H; among which the gross profit of 3Q2019 was HKD 462 million (corresponding period in 2018: HKD 373 million), representing an increase of 24% YoY. Direct costs and operating expenses in 3Q2019 was HKD 911.84 million (corresponding period in 2018: HKD 663.93 million), representing an increase of 37% YoY; the increase was mainly due to the increase in construction cost arising from the increased construction services, which contributed to a construction revenue of HKD 684.78 million in 3Q2019 as compared to HKD 491.71 million in 3Q2018. The GP margin was in 3Q2019 decreased to 34% (corresponding period in 2018: 36%), it was mainly due to a slightly larger proportion of construction revenue recognized in the mix of the total revenue of 3Q2019 as compared with 3Q2018; construction revenue comprised approximately 57% of total revenue in 3Q2019 (corresponding period in 2018: 54%).

The net profit attributable to shareholders in 9M2019 was HKD 603 million (corresponding period in 2018: HKD 515 million), increase of 17.1% YoY and 3.7 pts compared with 2019H; among which in 3Q2019 was HKD 183 million (corresponding period in 2018: HKD 144 million), representing an increase of 27% YoY. The net profit attributable to shareholders exceed our expectations, which is mainly due to effective control of costs.

Secures two waste water treatment projects in Shandong province, stable growth in production capacity

As at November 2019, the company has secured Shandong Ji`nan Tangye New Area Waste Water Treatment PPP project, which will be invested in, constructed and operated by a project company jointlyestablished and led by the company based on a PPP (Public-private Partnership) model, with a concession period of 30 years. The company holds a 99.9% stake in the project company. The project has a total designed daily waste water treatment capacity of 45,000 m3, with a total investment of approximately RMB 313 million. Additionally, the company entered into an agreement with the Management Committee of Shandong Zibo Economic Development Zone and secured Zibo Northern Expansion Project. The project will be invested in and constructed based on a BOT (Build-Operate-Transfer) model, with an investment of approximately RMB 83 million for a concession period of 30 years. Its designed daily waste water treatment capacity is 20,000 m3. The waste water treatment capacity remain growing stably, which is expected to enhance businesses through outstanding M&A projects.

Maintain "BUY" Rating

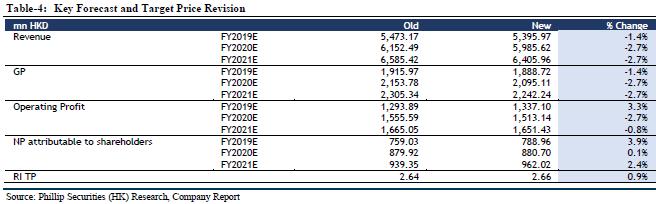

We adjusted our forecast for FY19/FY20/FY21 incomes to HKD 5.396/5.986/6.406 billion, showing increases of 13.16%/10.93%/7.02% YoY; net profit attributable to shareholders were HKD 789/881/962 million, with increase of 16.63%/11.63%/9.23% YoY; the corresponding EPS was HKD 0.2874/0.3185/0.3453. The target price was adjusted to HKD 2.66, corresponding to FY19/FY20/FY21 9.26x/8.35x/7.70x PE, which was +46.98% higher than the current price (HKD 1.81 as of November 15, 2019), maintaining a “BUY” rating.

Risk

Project progress fail expectations; Industry policy; M&A fails expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()