-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ANTA SPORTS (2020.HK) - Q3 Sales in line with expectation. Significant growth from online

Friday, October 23, 2020  21646

21646

ANTA SPORTS(2020)

| Recommendation | Accumulate |

| Price on Recommendation Date | $88.900 |

| Target Price | $94.900 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Q3 operating performance is in line with market expectations

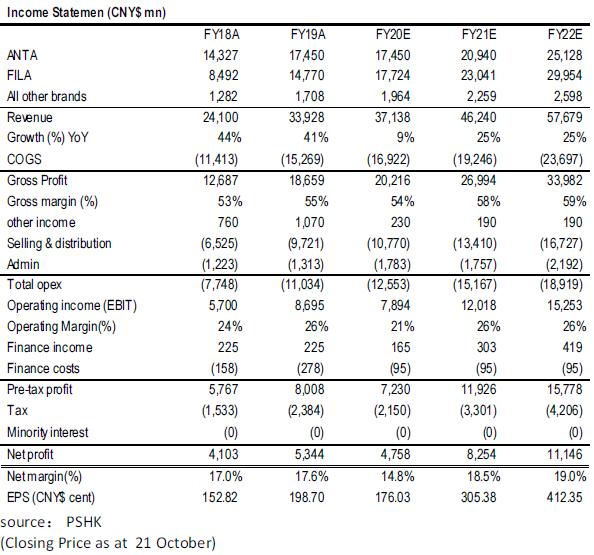

The company announced its operating performance for the 3Q20 on October 15th. As the epidemic situation eases, the company's operating conditions continue to improve. With the exception of AMER, the sales of all brands have recorded positive growth compared with the same period in 2019, which is in line with our expectations. The Anta brand recorded a low single-digit positive growth YoY. The FILA brand recorded a positive growth of 20%-25% YoY. Other brands recorded a positive growth of 50%-55% YoY.

Both online and offline efforts, Anta adult recorded positive growth

The overall turnover of the Anta brand recorded a positive single-digit growth. Among them, Anta adult achieved positive growth in Q3. The YoY growth of Q1/Q2/Q3 was 20% + negative growth/negative low single digit/positive growth respectively. Anta Kid achieved low double-digit growth. In terms of channels, the Anta brand's online sales growth has been impressive, with an increase of nearly 50% in Q3, and the growth rate has increased. In terms of discounts and inventory sale rate, affected by the epidemic and DTC transformation, the Anta brand discount rate increased by 2-3 ppt compared with the same period last year, and the discount rate was about 30% off. The inventory sale rate was unchanged MoM, approximately 6 times, and is expected to be controlled at approximately 5 times at the end of the year.

FILA's online and offline are developing simultaneously. FILA's online sale growth rate reached 90%, and the overall growth in Q3 was 20%-25%. Among them, FILA Fusion grew significantly, recording double-digit growth compared YoY, and offline growth was about 50%. %, and the online gross billing amount of Kid's clothing also increased by about 30%. In terms of discount and inventory-sales ratio, FILA discount is about 80%, and inventory-sales ratio is about 8 times.

Other brands recorded a 50%-55% increase in overall sales in Q3. Among them, the sales from the Descente increased by nearly 90% YoY, while Kolon Sport also recorded a YoY growth of 20%-25%. Winter products account for the majority of the product matrix of the two brands, and it is expected that the growth in Q4 will further increase.

AMER's overall turnover in Q3 was negative and low double-digit YoY, and it recorded a turnover growth of more than 20% in the Greater China region, which was better than expected. Under the company's expense management, it is expected to record profits throughout the year.

DTC transformation is progressing well

The transformation of the DTC model of Anta's main brand is progressing smoothly. As of 3Q20, the company has collected nearly 800 stores and change it to direct operation. In the short term, the transformation will incur additional costs for the company, but in the long term, flat and direct sales channels will help the company better grasp the retail data and market conditions. After the integration is completed, it is expected to further accelerate the destocking.

Valuation and investment advice

The Q3 operating data reflects the company's operating capabilities and resilience as a leader in the industry, and the overall performance is in line with our previous forecast. During the National Day and Mid-Autumn Festival this year, the company's entire brand recorded a growth of more than 40%, and its performance was better than that of the Labour Day Golden Week after the lockdown release, mainly because the overall consumption environment continued to pick up. At the same time, the cold winter came earlier this year, and demand for seasonal changes drives consumption. It is expected that Q4 will further improve operating data.

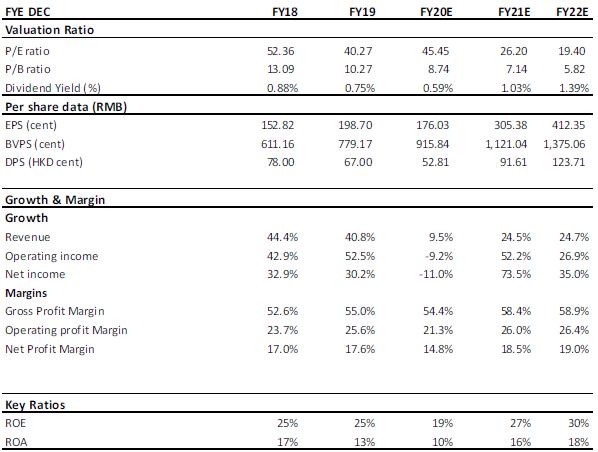

We maintain our earnings forecast and expect the company's 2020/2021 EPS to be RMB 1.76/3.05/4.12. The 12-month target price of HK$94.9 corresponds to the expected P/E of 48.53/28.00/20.50 times for 2020/2021. Comparing to the current share price, it is downgraded to the Accumulate rating. (Closing Price as at 21 October)

Risk

1) The impact of COVID-19 continues

2) The conflict between US and China

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()