-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Jonjee Hi-Tech (600872.CH) - Expand Both Capacity and Channels to Further Contribute to the Profits

Tuesday, January 23, 2018  15414

15414

Jonjee Hi-Tech(600872)

| Recommendation | Accumulate |

| Price on Recommendation Date | $27.150 |

| Target Price | $30.100 |

Weekly Special - 3306 JNBY Design Limited

Investment Thesis

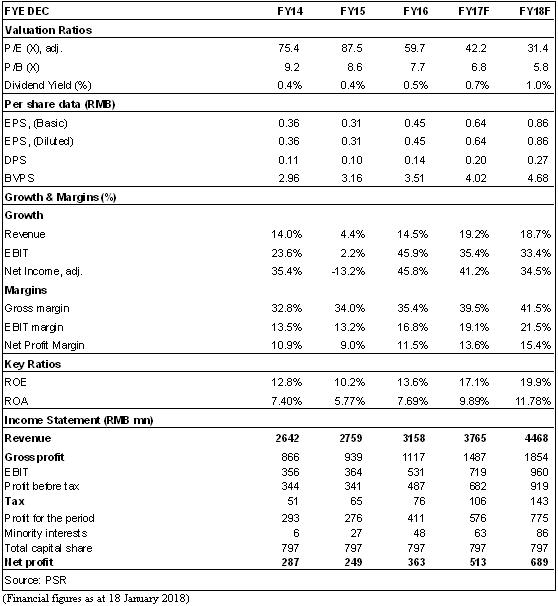

Jonjee Hi-Tech is a Leading Company in the Condiment Industry of China. Condiment industry is encouraged by the Chinese government, and enjoys huge market demand and broad development prospects. In the future, it will continue to benefit from the rise of the sales structure caused by the sales upgrading. With strong brand advantage, continuous expansion of production scale and channels, the company will keep consolidating its position in the industry, and its operating efficiency will still be on a steady growing trend. We expected diluted EPS of the Company to RMB 0.64 and 0.86 of 2016/2017. And we accordingly gave the target price to 30.1, respectively 35x P/E for 2018. "Accumulate" rating. (Closing price as at 18 Jan 2018)

Company profile: Leading Company in the Condiment Industry

Jonjee Hi-Tech is the first listed company among the 53 state-level high-tech zones in China, and also the first listed company in Zhongshan City. The company was established in 1993, and listed on the main board of Shanghai Stock Exchange in 1995. Jonjee Hi-Tech owns Guangdong Meiweixian Flavoring Foods Co., Ltd., Guangdong Zhonghui Hechuang Real Estate Co., Ltd., Jonjee Precision Machinery Co., Ltd. and other subsidiaries, of which the condiment business occupies the largest proportion, and accounts for about 95% of the total revenue and gross profit contributions.

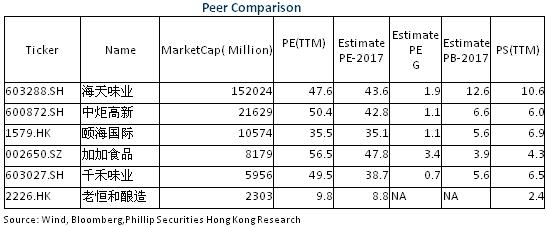

The company has a long history of producing soy sauce. Originated from Xiangshan Sauce Garden in the late Qing Dynasty and the early Republic of China, the company has won the title of "The Old Chinese Brand" and other national honors. The main products include the condiments (including soy sauce, chicken powder, oyster sauce, fermented bean curd, sauces, monosodium glutamate, vinegar, chicken bouillon and cooking wine), cooking oil and canned foods. The company is involved in production and sales of more than 100 varieties in 11 categories. The company is leading in the production technology in China, and the current overall production capacity exceeds 400,000 tons per year, of which sales of soy sauce account for nearly 70% of the total condiment sales. In addition, the production scale and market share rank second in China, only following Haitian (2.12 million tons); the sales of chicken powder account for 10-15% while the sales of other condiments account for 10-15%.

Advance Brand Construction, Channel Expansion and Capacity Improvement Strategies

1. Brand:

The company has adopted a two-brand strategy, and owns two major brands, "Chubang" and "Meiweixian". Specifically, Chubang is targeted at the middle and high-end market and its soy sauce has a 1.3g/ml amino acid nitrogen content, higher than the national standard by 85%, which makes it a product with high freshness. Chubang focuses on the consumption upgrade and is the core product of the company. Meiweixian is targeted at the low-end market, and focuses on the cost-effective advantage. In recent years, the company has launched a series of new products such as cooking oil, canned foods, cooking wine, rice vinegar and seasoning sauce. The company plans to gradually develop from soy sauce condiment to whole product lines. Concerning the brand marketing strategy, it also actively learns from international giants, and sponsors the foods entertainment TV show called Xianchu Dangdao, which we think will help further enhance the reputation and popularity of the company's "Chubang" brand.

2. Channels:

The company takes the distributorship-based marketing mode supplemented by direct sales, and strives to maximize product coverage on the market end; the direct sales business was mainly carried out in the Pearl River Delta; concerning the final product use, about 80% of its products are purchased and consumed by families while the rest is consumed by the restaurant business. Currently, the company is stepping up efforts to expand the restaurant market, and strives to gradually increase the proportion in the food and beverage consumption channels from the current 20% to 40%. China's southeast coast (Guangdong, Zhejiang, Hainan, Guangxi, Fujian, etc.) is the company's main marketing region where the company occupies a higher market share. The north and mid-west regions will be the focus of future channel expansion. The company divides the national market into five levels, adopts a differentiated marketing policy and gradually expands in a targeted manner. We believe the future potential of these low coverage regions is huge and these regions are expected to be an important support for the future growth of the company's sales volume in exceeding the industry's average growth.

3. Capacity:

The company currently owns two major production plants, Zhongshan and Yangxi. Concerning Zhongshan plant, the total capacity is 310,000 tons, the annual output of soy sauce is about 220,000 tons and the capacity utilization rate is 100%. The construction of the first phase of Yangxi plant was commenced in 2012 and the production capacity of 200,000 tons of soy sauce was put into operation in 2014. In addition, the 200,000-ton production facilities of soy sauce in the second phase are under construction. It is estimated that production will commence in 2018 and reach full production capacity in 2020. In addition, Yangxi plant also plans to build the 650,000-ton non-soy sauce production facilities under the mode of simultaneous construction and production. It is estimated to reach the full production capacity in 2023, providing a guarantee for the company's regional expansion. It is noteworthy that, compared with Zhongshan plant with obsolete facilities and high unit cost, Yangxi plant has high automation rate and its production efficiency is significantly higher than that of Zhongshan plant. We expect that the scale effect will further appear as the new production capacity is gradually put into production, which will boost the company's profitability to a higher level.

Stably-Growing Operation Data, and Accelerated Growth in the First Three Quarters of 2017

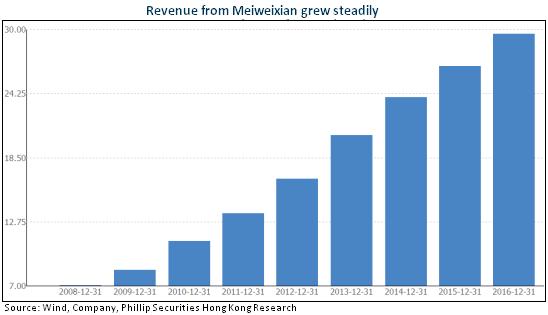

Benefited from the rapid development of the condiment business, the operating income of the company has maintained a good expansion tendency in recent years. From 2011 to 2016, the compound annual growth rate of operating income was 23%. In the first three quarters of 2017, the company achieved a total revenue of RMB2.729 billion, increasing by 18.84% yoy and maintaining a relatively rapid growth rate. In addition, the company recorded a net profit attributable to parent of RMB0.355 billion, increasing by 38.55% yoy. The equivalent EPS was RMB0.45, and the weighted average return on net assets was 12.1%, increasing by 2.3% yoy.

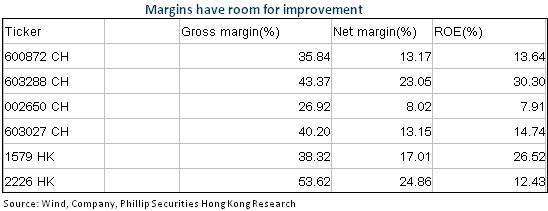

Specifically, the revenue of the subsidiary Meiweixian in the first three quarters was RMB2.65 billion, increasing by 22% yoy, and the net profit was RMB0.394 billion, soared by 46% yoy. Benefited from product price increases in Q1, the production efficiency improvement and product structure optimization in Yangxi plant, the gross profit margin reached 39.87%, increasing by 2.67%; the gross profit margin for the third quarter reached 41.3%, creating a record high. The period cost rate in the first three quarters was 23.66%, up by 0.8% compared to the first three quarters of 2016, which was mainly due to the increase in marketing expenses, leading to a 2.93% increase in sales cost rate.

Strong BS with sufficient cash flow

With the rapid expansion of its business scale in recent years, the demand for funds has been steadily increasing and the scale of liabilities has expanded. The Liability/Asset ratio increased from 36.7% in 2011 to 37.1% at the end of 2016 and 37.9% in 2017, but still maintained at a low level. The Company's cash management from the food segment is strong, operating cashflow+from+sales+of+goods /revenue ratio is maintained at a good level, and the sufficient operating cash flow provides a strong guarantee for debt repayment.

Risk

Price war among peers

Raw material price increase

New business risk

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()