-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Wisdom Education (6068.HK) - Benefited from Greater Bay Area, Positive on Private education in Guangdong

Thursday, July 19, 2018  9462

9462

Wisdom Education(6068)

| Recommendation | Accumulate |

| Price on Recommendation Date | $6.900 |

| Target Price | $7.810 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Wisdom education mainly provides private premium education, including elementary, middle, high schools and international programmes in South China in Dongguan, Huizhou, Panjin, Weifang and Jieyang respectively. Thanks to the robust growth in Guangdong's economy, the future development of Greater Bay Area and its high quality of education, we believe Wisdom will become the fastest growth K12 operators in the China education sector. Thus, we initiate an “Accumulate” rating on Wisdom, and a target price of HK$7.81 based on earnings in 19F assuming 1x PEG (35% CAGR on earnings for FY18E-20E), with 13.2% potential upside. (Closing price at 16 Jul 2018)

Company Background

Founded in 2003, Wisdom is operating 7 schools in Dongguan, Huizhou, Jieyang, Weifang, and Panjin and providing private premium education for PRC curriculum programmes, including elementary, middle, high schools. Besides domestic curriculum, Wisdom also provides international programmes for high school students. It offers a wide-range of courses for students, such as sports, art, music and Chinese culture, in order to facilitate the well-rounded development of students.

1) Dongguan Guangming Secondary School

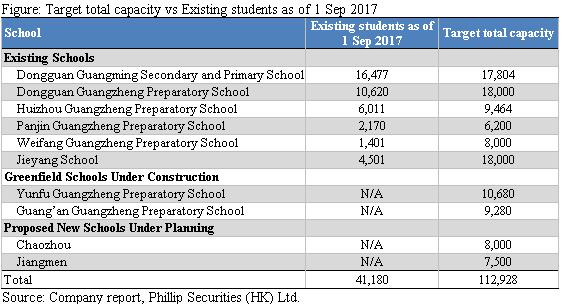

Established in 2003, the school is located Dongguan and offers both PRC curriculum programmes and international programmes. As of 1 Sep 2017, it had 10,507 students for middle and high school sections. The school's total developed site area was approximately 137,645.2 sq.m., and is located on the same campus site as Dongguan Guangming Primary School.

2) Dongguan Guangming Primary School

Established in 2004, the school is located Dongguan and only offers primary school education. As of 1 Sep 2017, it had 5,970 students. The school provides spoken English courses to all students in order to encourage students` proficiency in English. The school's total developed site area was approximately 24,192.0 sq.m., and is located on the same campus site as Dongguan Guangming School.

3) Dongguan Guangzheng Preparatory School

The school was called “H.S. Kama International School” previously, and changed to current name after acquisition in 2013. It is located Dongguan and offers both PRC curriculum programmes and international programmes. 10,620 students enrolled for primary, middle and high school sections as of 1 Sep 2017. The total developed site area of the school is developed is approximately 193,265.3 sq.m..

4) Huizhou Guangzheng Preparatory School

Established in 2014, the school is located in Huizhou and provides primary, middle and secondary school education. The school had 6,011 students for primary, middle and high school sections as of 1 Sep 2017. The total developed site area of the school was approximately 64,321.1 sq.m..

5) Panjin Guangzheng Preparatory School

Commenced in 2014, the school is located in Panjin and provides primary, middle and secondary school education. As of 1 September 2017, the school had a total student enrolment of 2,170 for primary, middle and high school sections. The total developed site area of the school is approximately 206,340.7 sq.m., and has a spacious football court on campus, offering football classes to students as football is a popular sport in Liaoning province.

6) Weifang Guangzheng Preparatory School

Started operating in 2016, the school is located Weifang with primary, middle and secondary school education. As of 1 September 2017, the school had a total student enrolment of 1,401, together with approximately 104,758 sq.m. of developed site area.

7) Huanan Shida Yuedong Preparatory School (Jieyang School)

The school is located in Jieyang, and acquired 65% equity interest by Wisdom in September 2017. It offers primary, middle and secondary education. As of 1 September 2017, the school had a total student enrolment of 4,501 for primary, middle and high school sections.

The student enrollment as of 1 Sep climbed from 19,354 in 2013 to 41,180 in FY17, with a CAGR of 21% YoY. The proportion of the middle school students remains the largest section, around 40% during FY13-17, demonstrating the importance of middle schools section to Wisdom. The utilization rate dropped significantly to 82.7% in FY17 due to the increase in capacity for Dongguan Guangzheng, Huizhou, Panjin and Weifang schools. Meanwhile, the number of teacher was 2,580 as of 1 Sep 2017, and the teacher-student ratio remains around 1:16, indicating Wisdom has retained the ratio in order to provide high quality education. For the 2016/2017 school year, approximately 90% of Wisdom's primary school graduates were admitted to its middle schools together with approximately 60% of middle school graduates to its high schools.

The overall average tuition and boarding fees per students (ARPU) has increased by 6.1% to $21,114 RMB. All schools of Wisdom have raised its tuition fee in 2017, and Dongguan Guangming School had the largest increase among the schools, about 11.7%. Apart from tuition and boarding fees, the revenue from ancillary services hiked substantially to 308 million RMB in FY 17, 104.5% growth YoY, and its proportion of total revenue increased from 22% FY14 to 31.5% in FY 17, as Wisdom is eager to explore new source of revenue, and enhances the its service level to their students in the same time.

Industry Overview

Expanding market size of the private fundamental education in Guangdong thanks to economic development and rebounding birth rate

Due to the robust economic growth in Guangdong, the per capita disposable income of households has raised from $23,421 RMB in 2013 to $33,003 RMB in 2017, a CAGR of 9% during 2013-17. As the residents in Guangdong become wealthier, the parents may be more capable of sending their child to private schools that could provide higher quality education than public.

In 2016, the government replaced the One-child policy with Two-child policy. The birth rate in Guangdong increased hugely to 13.7% in 2017, higher than the past 13 years. And, the birth population was 1.51 million, increased by 0.22 million YoY. Although the birth rate in China dropped in 2017 instead, we are positive to the future birth rate in Guangdong because the households in Guangdong generally have better resource to raise more than a child than other less developed provinces. We expect many parents in Guangdong are more than willing to have more than a child once they are permitted by law.

Thanks to economic development and rebounding birth rate in Guangdong, we expected the market size of private education in Guangdong will be expanding.

According to Frost & Sullivan, it is estimated the total revenue of private fundamental education in Guangdong will reach 46.8 billion RMB in 2020, with a CAGR of 10.9% during 2016-20F. Private education operators will surely be benefited from this trend.

The rising private school penetration in primary and secondary education

Private school has played a more important part in the education sector. According to Frost & Sullivan, the penetration rate of elementary, middle, and high school has kept increasing during 2012-15. It is expected the rate will reach 8.9%/13.8%/12.8% for elementary/middle/high schools respectively in 2020F. The proliferation of private schools can be attributed to its higher quality of education than public schools. Private schools usually had a greater motivation for improvements, as they are motivated to react towards the market and provide high quality teaching in order to charge higher tuition fees; while the actions of public schools are usually guided by government. Besides, private schools could adjust and diversify its curriculum to provide a broader and flexible curriculum, attracting high quality students, but public schools is limited due to the requirements of governmental departments.

Entry barrier

Lengthy and complex regulatory approvals from government

In order to establish a private school in China, the operators need to comply with the Education Law of the PRC, the Law for Promoting Private Education and the Implementation Rules for the Law of Promoting Private Education of the PRC, which is considered to be lengthy and complex, creating an entry barrier to the potential operators.

High capital requirement

The establishment of private schools requires high initial capital expenditure in both land use right and campus. The on-going investment is also needed, for example renovation or facilities upgrade, thereby posing an entry barrier to new operators.

Availability of land

Sufficient area of land is crucial for school establishment and development, as the area directly affect the class size and the quality of education. The difficulty of acquiring land has been manifested across developed cities due to the skyrocketed price of land. Thus, it could form an entry barrier for the existing school operators.

Prohibition for foreign investors

According to Foreign Investment Industries Guidance Catalog (Amended in 2015), foreign investors are prohibited from investing primary and middle school. They are only allowed to invest in preschool, high school, and high education by cooperating with domestic parties, where domestic parties should play the dominant role. The prohibition for foreign investors could reduce the competition from oversea, protecting the existing operators in the industry.

Long term growth drivers

Locating in top cities in Guangdong, benefited from Guangdong-Hong Kong-Macao Greater Bay Area

Guangdong-Hong Kong-Macao Greater Bay Area is a plan for the development of a city cluster in the Guangdong, including Hong Kong, Macau, Guangzhou, Shenzhen, Zhuhai, Foshan, Zhongshan, Dongguan, Zhaoqing, Huizhou and Jiangmen. The Greater Bay Area has become one of the key development strategies for China and will lead to the inflow of labors with strong competitiveness to Guangdong. We believe the demand for private premium education can be boosted by both the economic development and the inflow of talents.

Currently, 4 out of 7 schools are located in the Greater Bay Area, which are Dongguan Guangming Secondary, Dongguan Guangming Primary, Dongguan Guangzheng and Huizhou Guangzheng. And, Wisdom confirmed to establish a school in Jiangmen, but yet to disclose the expected year of opening. Besides, Wisdom's schools in Jieyang, Chaozhou, and Yunfu are nearby the Greater Bay Area, so it should be benefited even if those schools are not exactly located in the Greater Bay Area. The mgt confirmed they will focus on Guangdong, in order to seize this opportunity in the Greater Bay Area.

Brand effect spilling out with replicating operation model

Dongguan Guangming Secondary and Primary School is currently one of the top schools in Guangdong. In 2017/2018, almost 20,000 students applied for the 900 primary one places, demonstrating a high recognition from parents. We believe the brand effect of Wisdom in Guangming could be spilled out if its operation model can be replicated to schools in other cities. In order to do this, Wisdom sends its mgt staff from old schools to new one, implementing its operation models in new schools. Besides, it standardizes teacher recruitment criteria to ensure the education quality for their schools. In 2017 PRC national higher education entrance examination, 4 out of 10 students admitted to Tsinghua University were from schools other than Dongguan Guangming Schools (3 for Huizhou Guangzheng and 1 for Dongguan Guangzheng), indicating the success in Dongguan Guangming school was gradually shown in other schools.

Excellent graduation track record

Parents pay expensive tuition fee for high quality of education, so we believe the quality of education is one of the crucial competitive edges for private education operators. For past four schools years (2013/14, 2014/15, 2015/16 and 2016/17), over 90% of Wisdom's high school graduates were admitted to universities in China. In 2016/17, around 25% of its graduates were admitted to first-tier universities in China identified in the“University Application and Enrolment Guidelines for Guangdong Province” issued by the Education Examinations Authority of Guangdong Province. Besides, Wisdom's graduates also accomplish remarkable achievements. In both 2016 & 2017 PRC national higher education entrance examination, 10 graduates were admitted to Peking University and Tsinghua University. Moreover, one of its high school graduates was ranked in the top 10 and one was ranked in the top 20 in Guangdong province in terms of the total exam scores achieved in 2016. Wisdom's excellent graduation track record indicates its high quality of education, which differentiates Wisdom from other private education operators.

Sufficient capacity for upcoming demand

Except Dongguan Guangming Secondary and Primary School, Wisdom's schools all have sufficient land to expand in order to cope with the upcoming demand. Although Dongguan Guangming Secondary and Primary School has no extra land for expansion, Wisdom has purchased a campus that is near Dongguan Guangming to serve as a its additional campus, which is expected to increase the capacity by 1,000. The target total capacity (in case all the land has been developed) is 112,928, while the existing students as of 1 Sep 2017 is 41,180, referring the utilization rate is only 37%. It indicates that even if there is no new greenfield schools or acquisitions, Wisdom still has sufficient capacity to deal with the upcoming demand.

Increasing proportion on Ancillary services

As all Wisdom's schools are boarding school, students must stay on the campus for long period. Wisdom provides as many ancillary services as possible, such as Supermarket, School bus, School uniform purchase, or Study tour, so that it can create new source of revenue other than tuition and boarding fees. With the rise of student enrollment, the revenue of ancillary services should climb correspondingly. The mgt predicts that the proportion of ancillary services to total revenue could reach 40% ultimately.

Earnings forecast

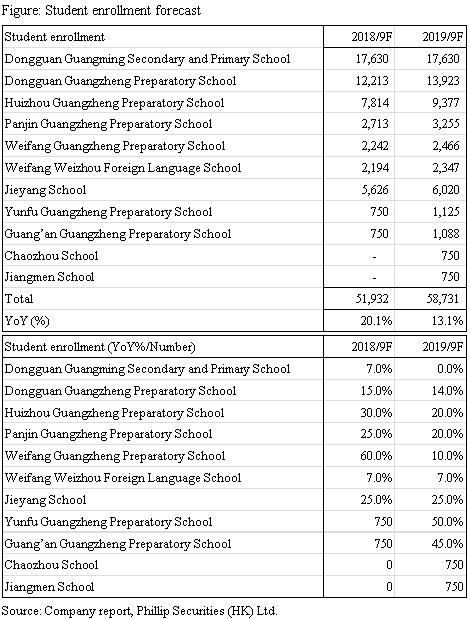

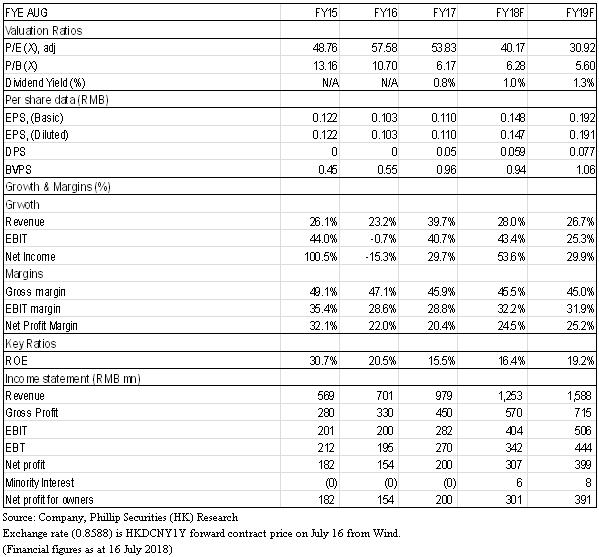

We forecast the students enrollment to be 51,932/58,731 in FY18/19, with 20.1%/13.1% YoY.

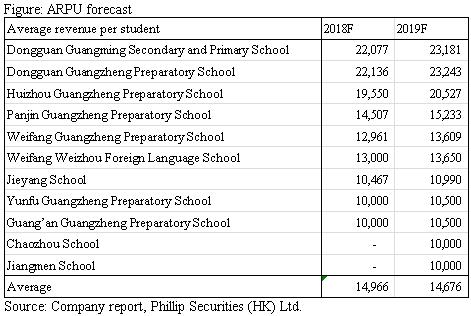

We expect the ARPU will rise around 5%, as Wisdom confirmed they will raise the tuition fee in school year 18/19, which will reflect in financial year of 2019.

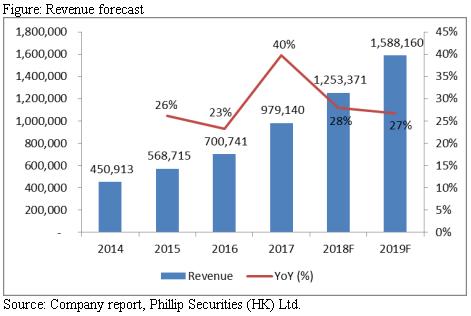

We projected the revenue to be 1.25/1.59 billion RMB, with the growth of 28%/27% in 2018/19F.

Since the GPM of ancillary services is lower than tuition, as we expected the GPM to drop to 45.5%/45% with the increasing proportion of ancillary services.

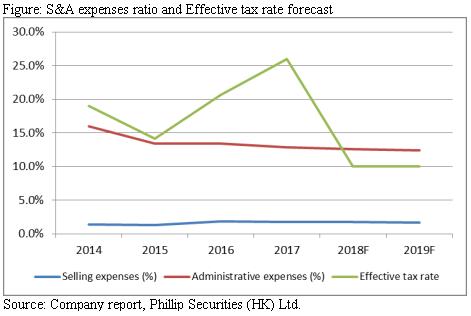

Thanks to the operating leverage, we expect the selling expenses ratio to be 1.6%/1.5% in 2018/19F; while the administrative expenses ratio to be 12.6%/12.4% in 2018/19F. Wisdom has categized its schools to be not-for-profit, so we predicted the effective tax rate to be 10% in both 2018/19F.

Valuation

Thanks to the robust growth in Guangdong's economy, the future development of Greater Bay Area and its high quality of education, we believe Wisdom will become the fastest growth K12 operators in the China education sector. Thus, we initiate an “Accumulate” rating on Wisdom, and a target price of HK$7.81 based on earnings in 19F assuming 1x PEG (35% CAGR on earnings for FY18E-20E), with 13.2% potential upside. (CNY/HKD = 1.16)

Risk

1. VIE structure prohibited in China

2. New acquired schools were not able to add value

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()