-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

SIA (600009.CH) - The Overall Listing Plan Price Is Determined and the Results Are Approaching an Inflection Point

Thursday, March 3, 2022  1419

1419

SIA

| Recommendation | Accumulate |

| Price on Recommendation Date | $54.160 |

| Target Price | $62.300 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

2021 Review

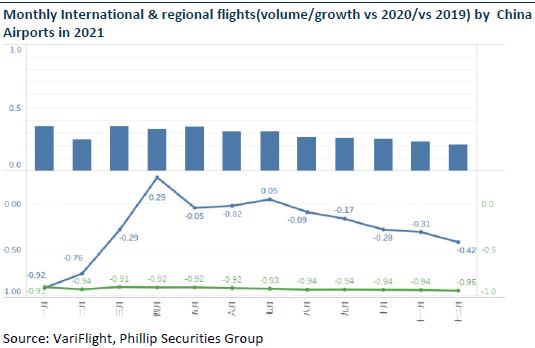

Under the influence of the pandemic, the passenger throughput of airports in China reached 907 million in 2021, an increase of 5.9% over 2020, and a recovery of 67.1% in 2019, which was a 32.9% decline compared to 2019. On a closer look at markets, due to the Spring Festival travel policy and the repeated sporadic outbreaks in China, the low point of aviation demand for domestic routes appeared in February, August and November, and the high point was in March, April, May and July. As the Civil Aviation Administration of China enforced strict control over the cases imported from overseas, the number of international and regional flights has always hit a trough, with small fluctuations throughout the year. Compared to 2019, the monthly number of international and regional flights has dropped by more than 90%. Only the number of flights in April and July increased slightly compared to 2020.

In 2021, SIA reported a passenger throughput of 32,210 thousand, up 5.7% yoy, slightly weaker than the industry's overall 5.9%, and a sharp drop of 57.7% compared to 2019. Specifically, the passenger throughput of domestic routes reached 30,530 thousand, up 19.2% yoy, and down 18.9% compared to 2019. The passenger throughput of international and regional routes registered 1,679 thousand, down 65.5% yoy and down 95.6% compared to 2019. However, driven by the strong cargo demand, the Company recorded an annual cargo and mail throughput of approximately 3,990 thousand tons in 2021, an increase of 8.1% over the same period in 2020, and an increase of 9.7% over the same period in 2019..

Compared to other airports in China, Shanghai Pudong International Airport is more dependent on non-aviation revenue such as international routes and duty-free business rentals in terms of results. Therefore, the sharp drop in international passenger traffic has a greater impact on the airport's results. According to the result forecast released on 24 January 2022, the Company predicted losses in 2021 could reach RMB1.64 billion to RMB1.78 billion. The corresponding loss from Q1 to Q4 was RMB436 million, RMB304 million, RMB510 million and RMB390-540 million. The annual tax-free revenue was expected to approach RMB500 million, a decrease of nearly 90% compared to nearly RMB5 billion in 2019.

Mild Recovery Continues in Early 2022

However, with the improvement of the pandemic situation and the relaxation of travel restrictions in China, the overall domestic aviation demand showed a trend of strong resilience and rapid recovery. In January 2022, there were 599,476 aircraft movements of passenger flights at airports in China, up 1.7% from 2021, up 11.78% from December, and down 25.28% compared to January 2019. Specifically, the recovery of domestic flights improved compared to the previous month. The aircraft movements increased by 11.84% from December, up 0.66% from 2021, and down 17.46% from 2019. However, the aircraft movements of international and regional flights climbed by 4.28% from December, down 41.66% from 2021, and down 95.07% from 2019. There was still no obvious sign of recovery.

According to SIA's announcement, there were 29,735 aircraft movements in January, up 13.99% yoy; the passenger throughput was 2,118.3 thousand, up 14.47% yoy; the cargo and mail throughput was 318.7 thousand tons, down 10.43% yoy.Recently, the government announced the 14th Five-Year Plan for the civil aviation industry, in which 2021~2022 is defined as the recovery period and accumulation period of China's civil aviation industry, while 2023~2025 is the growth period and acceleration period. The focus will be on expanding the domestic market and restoring the international market, and vigorously developing the cargo market. We expect 2022 to become an inflection point in the results of airport companies, and 2023 will start a rebound in results.

The Overall Listing Plan for RMB19.1 Billion Asset Injection Is Determined

According to the announcement, SIA signed an agreement with the holding major shareholder SAA, in which the transaction price of 100% equity of the underlying asset Hongqiao Airport is approximately RMB14.5 billion, the transaction price of 100% equity of the logistics company is approximately RMB3.1 billion, and the transaction price of No.4 Runway in Pudong Airport is approximately RMB1.5 billion, with a total of approximately RMB19.1 billion. The listed company is expected to issue approximately 434 million shares to SAA at a price of RMB44.09 per share. Meanwhile, the Company will issue no more than approximately 128 million targeted additional shares to SAA. The scale of supporting financing will be reduced to no more than RMB5 billion. The issue price will be RMB39.19 per share. The raised funds are planned to be used for the Company's four-type airport construction project, smart cargo terminal project, comprehensive improvement project of smart logistics park and working capital supplement. After the transaction is completed, SAA will hold 58.38% of the total share capital of the listed company (46.25% before the transaction).

We think that Hongqiao Airport, which mainly engages in domestic routes, has quick business recovery. In the long run, it has good development prospects and strong profitability. The injection into the listed company will realise the re-integration and optimization of route resources. Affected by the pandemic, Pudong Airport, which mainly focuses on international routes, has high operating costs. In order to utilize resources more rationally and efficiently, Shanghai Airport has tried to divert a large number of idle international time resources to the domestic market, so that the passenger flow of Pudong Airport will recover faster. In addition, the reorganisation will also incorporate the logistics and cargo business, which will help improve the air cargo hub network, expand multimodal transportation, and optimize the cargo layout of Hongqiao Airport and Pudong Airport.

Investment Thesis

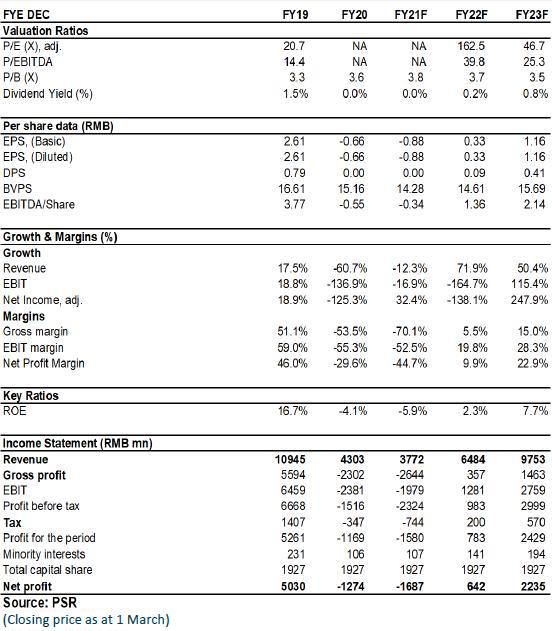

We think that with the progress of vaccines, although there will still be challenges and setbacks, the dawn of the road to recovery has been clear, the airport encumbered by the pandemic has passed the darkest period, and the future performance of the Company is more inclined to grow than decline. In addition, as the injection of additional assets has not yet been completed, the relevant impact will not be considered for the time being. We revised the EBITDA predicted value of SIA in 2021/2022/2023, and revised the target price to RMB 62.3 (formerly RMB 56.3), and the "Accumulate" rating is given. (Closing price as at 1 March)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()