-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

INVESTNOTES REPORTS REVIEW

Friday, July 3, 2020  20281

20281

INVESTNOTES REPORTS REVIEW

Weekly Special - 3306 JNBY Design Limited

Sectors:

Air & Automobiles (Zhang Jing),

Automobile & Air (ZhangJing)

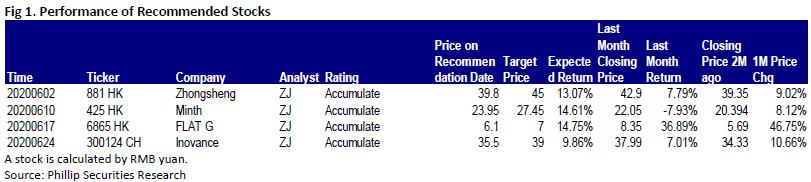

This month I released 4 updated reports of Zhongsheng (881.HK), Minth(425.HK), FLAT Glass (6865.HK) and Inovance (300124.CH), which got success by their unique Competitive edge. Among them, we highly recommend FLAT Glass (6865.HK).

In 2019, the sales volume of PV glass of the Company reached 160 million square meters, up by 67% yoy. The gross margin of the Company increased by 5.18 ppts to 32.87% because of the recovering price of PV glass, improvement of production efficiency of the newly-commissioned production capacity and improvement of product mix (thin glass accounted for a higher proportion). The proportion of revenue from PV glass increased to 78%, approaching 80%. Total production capacity increased to 5400 tons/day.

Flat Glass recorded a revenue of RMB4,807 million in 2019, up by 56.9% yoy because of the rise of unit price resulting from commission of new production capacity and the recovery of demand, net profit attributable to the parent company of RMB717 million, up by 76% yoy.

In Q1 2020, the Company recorded a revenue of RMB1,203 million, up by 29.10% yoy; net profit of RMB215 million, up by 97.0% yoy. Because of the continuance of effect of price yoy lift of PV glass, plus with the low material price, 2020Q1 gross margin continued to hike, reaching a historic height of 39.88%.

In 2019, domestic PV market tightened, but great performance was reported in overseas market, with export increasing rapidly. Strong overseas momentum was continued in Q1 2020, which compensated the shortage of domestic demand due to domestic suspense of work. In Q2, the delay of overseas demand caused by the pandemic put pressure on the price of PV glass, which may exert some negative impact on the results of the Company in 2020 Q2. However, the revenue from European and American markets only accounted for 10% of the total revenue of the Company. We expected that the demand side will improve steadily from H2 because of the reopen. Looking forward, the PV industry has entered the phase of scale competition. The concentration of the industry continuously roused, and the total market share of the Company and Xinyi Solar has exceeded 50%, which helped the double-oligarchy layout taking shape.

Recently, the Company announced that it would release convertible bonds of RMB1.45 billion and Private placement of RMB2 billion, which were mainly used in the production and construction of the two 1,200-ton-per-day production lines (Line 4/Line 5), as well the preparation and construction of Line 6/ Line 7 (also 1,200 tons per day) in Fengyang, Anhui. Due to obvious advantages in technology and scale of newly increased capacity, increase in finished production rate and decrease in unit cost will further improve the profitability of the Company.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()