-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

LI NING (2331.HK) - 2020 performance is in line with expectations, operating efficiency continues to improve

Monday, April 19, 2021  7527

7527

LI NING(2331)

| Recommendation | Accumulate |

| Price on Recommendation Date | $57.800 |

| Target Price | $66.110 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

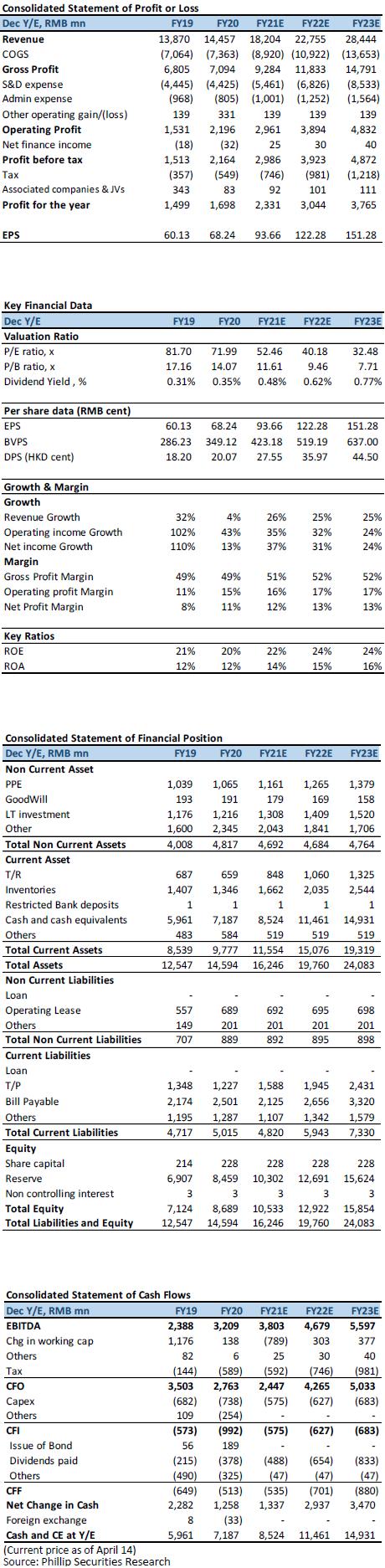

Li Ning announced on March 19 the company's annual results for the year ended December 31, 2020. The company's 2020 revenue was RMB 14.46 billion, an increase of 4.2% year-on-year, which was in line with our previous expectations (previous expectations: RMB 14.56 billion) , the annual net profit was 1.70 billion yuan, slightly better than our expectation (previously expected: 1.66 billion yuan), an increase of 13.3% year-on-year (including one-off non-operating gains of CNY 234 million in 2019). If the relevant items are excluded, the company Core attributable net profit increased by 34.2% year-on-year. NPM increased from 10.8% to 11.7%, an increase of 0.9 ppts year-on-year, mainly due to the company's proper control of operating costs. The company declared a final dividend of CNY 20.46 cent per share, with a full-year dividend payout ratio of approximately 29.6%.

The annual revenue growth MSD, and cost control offsets the impact of the epidemic

Li Ning's annual revenue was RMB 14.46 billion, an increase of 4.2% year-on-year. In terms of distribution channels, the company's revenue from retail/wholesale/e-commerce changed by 0.9%/-9.7%/29.9% year-on-year, accounting for 48%/23%/29%, respectively, and the proportion of revenue from e-commerce increased by 5 ppts to 29%. From the perspective of core categories, in terms of retail sell-through, the overall increase was 1% year-on-year compared to last year, but only sports casual recorded a positive growth, an increase of 23% year-on-year, accounting for 39%, and an increase of 7 ppts. Other core categories such as running/training/basketball/non-core are reduced by 9%/16%/4%/9% respectively, and the proportion of retail turnover is 17%/16%/26%/2%.

The company's net profit for the year was CNY 1.70 billion, a year-on-year increase of 34.2% based on core net profit, and a NPM of 11.7%, an increase of 0.9 ppts. The GPM was the same as last year, at 49.1%, mainly due to the company's adjustment of the wholesale business price increase during the year, which increased the GPM and offset the negative impact of increased discounts on the GPM due to the epidemic. During the year, the company controlled expenses appropriately, research expenses, advertising and market promotion expenses, and staff costs, accounting for 2.2%, 8.9%, and 9.1% of revenue, respectively, representing a year-on-year decrease of 0.4/0.7/ 1.8 ppts. From the perspective of operating, the company's inventory turnover days were 68 days, same as FY19, reflecting that the inventory of channels affected by the epidemic during the year has also been digested. During the year, the company also adjusted its channels and reduced its low-efficiency offline franchise stores. The total number of stores decreased by 617 year-on-year to 6,933 as of December 31, 2020.

Good performance in the 1Q21, conservative revenue guidance

For the FY21, the company expects sales growth of 20%-25%, while retail sell-through in various channels will increase by 18%-23%. On the profit side, the company expects to increase its NPM by 1 ppts in 2021. We believe that the company's guidance is relatively conservative. The company's offline retail sales from January to mid-March increased by about 70% year-on-year, compared to a 30% increase in 2019, and the recovery of offline channels is progressing well. As the brand image improves, the room for price increases on products will also be further expanded in the future.

Valuation and investment advice

The company's revenue and profit in FY20 were in line with our expectations. Under the epidemic, revenue still recorded a single-digit positive growth. In addition, cost control and price adjustments also offset the negative impact of discount promotions. With the improvement of operating capacity and the rise of the national trend, we maintain our previous expectation that the company's revenue growth in the next three years will be 25%. With the increase in the company's direct sales ratio and the establishment of brand image, the company's GPM is expected to increase year-on-year. The GPM in FY21/FY22 is expected to be 51%/52%. The company's earnings ratio is at a relatively high level in the industry, mainly because the market has higher expectations for the company's future growth, and the brand image also provides a premium for it, benchmarking against international sports brands. Considering that the company's brand has huge growth potential, profitability will be further improved in the future, and the future earnings growth potential is huge. We have raised the company's FY21/FY22 earnings per share to CNY 93.66/122.28 cents (previously: CNY 82.54/107.58 cents). Based on the company's future revenue growth higher than our previous expectations, we raise our target P/E to FY21 60x. Raise the target price to HKD 66.11, corresponding to 60.00/45.95 times expected earnings ratio in 2021/2022, corresponding to the current price, and maintain the Accumulate rating.

(Current price as of April 14)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()