-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

CEA (670.HK) - Oil Price/Exchange Trend Begins to Decompress Aviation Enterprises

Monday, January 21, 2019  6256

6256

CEA(670)

| Recommendation | Accumulate |

| Price on Recommendation Date | $4.620 |

| Target Price | $5.040 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary:

Over 40% Decrease in Profit in the First Three Quarters

According to CEA` report of the first three quarters (Chinese Accounting Standards) in 2018, in the first three quarters of 2018, the company recorded revenue of RMB87,878 million, up by 13.4% Y-o-Y, and a net profit attribute to the parent company of RMB4.49 billion, down by 43.3% Y-o-Y. Among them, during the third quarter, the company recorded revenue of RMB33,456 million, up by 13.5% Y-o-Y, and a net profit attribute to shareholders of RMB2,207 million, down by 38.1% Y-o-Y.

Dragged by Oil Price/Exchange Rate/Cardinal Number

Firstly, due to the rising international oil prices in the first three quarters of 2018, CEA` operating cost increased by 13.4% Y-o-Y due to the sharp rise in fuel cost. Specifically, the increase in operating cost in the third quarter reached 15.7%, which dragged down the operating profit.

Secondly, the exchange rate of RMB against US dollar has been depreciating continuously since the end of the second quarter of 2018. By the end of the third quarter, the exchange rate level has depreciated by 5.92% compared with that at the beginning of the year, which not only wiped out the 3.4% increase in the first quarter, but also set a new low since China's exchange rate reform. The devaluation resulted in a great increase in the exchange losses of CEA. The financial expenses in the second and third quarters soared by 983% and 692% Y-o-Y, respectively, to RMB2.95 billion and RMB2.55 billion, which greatly eroded the net profit.

Thirdly, during the same period last year, CEA sold 100% of its stock rights of Eastern Air Logistics Co., Ltd. (EAL), earning RMB1.75 billion one-time profits, and resulting in a higher Y-o-Y cardinal number.

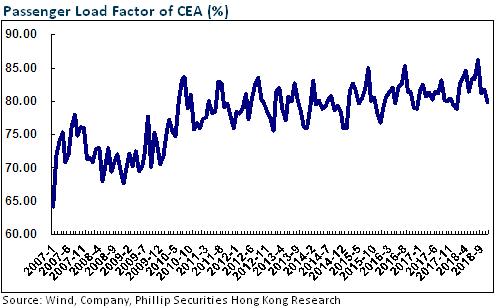

Under the Control of Capacity, Core Business Performance is Excellent with Rising P L/F

Benefiting from strong air demand in East China market, the demand of Xi`an/Kunming market recovered, and the main business of CEA increased significantly Y-o-Y. In the first three quarters of 2018, CEA completed 90.56 million passenger traffic, an increase of 9.6% Y-o-Y; RPK increased by 9.2% compared with the same period in the last year, with domestic, international and regional growth of 8.6%, 9.9% and 10.9%, respectively; ASK increased by 7.8% Y-o-Y, with domestic, international and regional growth of 8.4%, 6.9% and 7.8%, respectively. Additionally, the CAAC strictly controls the punctuality rate and flight time delivery, and the P L/F and fare level of CEA have risen: The P L/F during the period was 82.87%, up by 1.47 ppts Y-o-Y, which exceeds the P L/F of three major airlines; and the fare level has risen by 3.2% Y-o-Y.

Oil Price/Exchange Trend Begins to Decompress Aviation Enterprises

Since the fourth quarter of 2018, international oil prices have fallen by 30% from their peak, and the current level has also fallen by about 20% compared with that in the same period. It is expected that there will be little possibility of a sharp rise again. From the fourth quarter of 2018, the pressure on fuel costs of CEA will be greatly reduced.

In terms of exchange gains and losses, with the difficult progress of Sino-US trade negotiations, the RMB exchange rate in the fourth quarter of 2018 was stable and did not continue to depreciate. In the first quarter of 2019, the RMB exchange rate even showed a trend of appreciation, which was more than 1% higher than the cumulative appreciation at the end of last year. This will also greatly alleviate the pressure of exchange losses of the company.

Investment Thesis

As a pioneer in the reform of mixed ownership in domestic civil aviation industry, CEA recently announced the introduction of private placement to strategic investors Juneyao Air and Juneyao Group. The funds raised will be used to purchase 18 aircraft/15 simulators/20 standby engines. We hope that the two parties will further cooperate with each other in route synergy and improvement of operational efficiency in the future, to consolidate Shanghai's market share and enhance profitability.

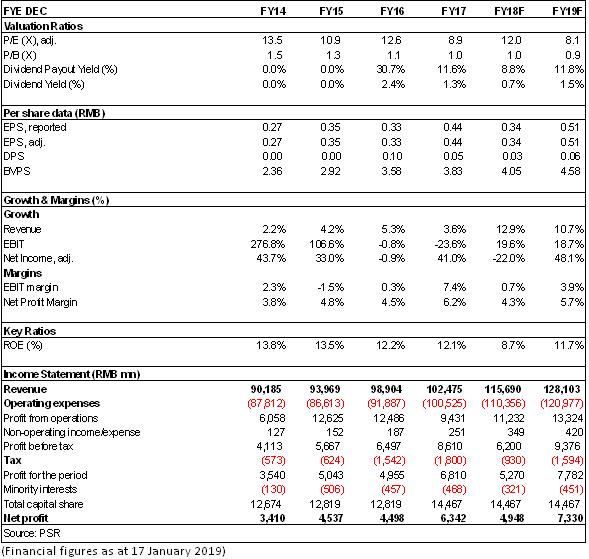

We expect the company's 2018/2019 EPS of RMB0.34/0.51. Given that possible improvement on efficiency after the mix reform, and the expected better ticket price in the future, we are optimistic about the Company's future result flexibility. Therefore, we set the target price at HK$5.04, equivalent to 13.1X/8.8X estimated P/E in 2018/2019. Also, the "Accumulate" rating is given. (Closing price as at 17 Jan 2019)

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Highspeed railway diversion

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()