-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CRL (1109.HK) - Fundamental factors kept improving

Monday, July 9, 2012  18519

18519

CRL(1109)

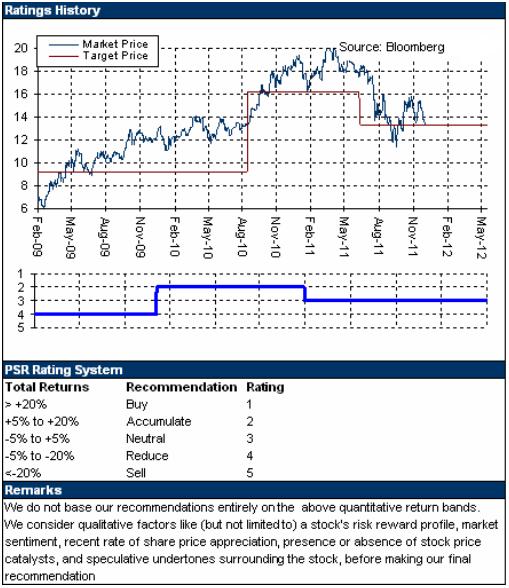

| Recommendation | Neutral |

| Price on Recommendation Date | $16.380 |

| Target Price | $16.200 |

Weekly Special - 3306 JNBY Design Limited

Summary

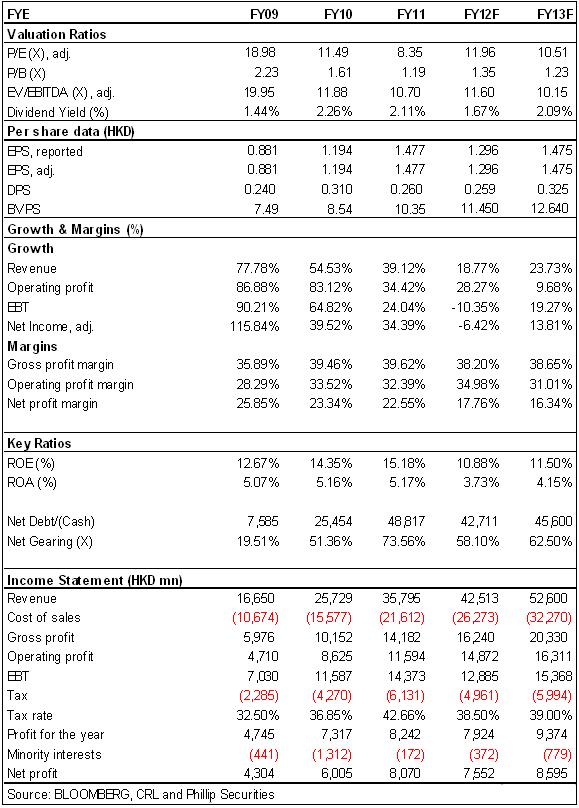

Contracted sales of CRL in 1H2012 increased sharply, exceeding market forecast. Its contracted sales in the first six months reached RMB 20.6bn, significantly rising by 56% than 13.2bn in 1H 2011, and accounted for 52% of full-year sales target of 40bn. CRL's completion rate was obviously better than peers average because the company launched more positive selling strategy and house market had been recovering. Its sales in May and June reached 5bn and 4.3bn with obvious improvement.

Since 2011 the company accelerated its steps on commercial properties, and several projects have been opened one by one. Because more capital was put into investment properties, more projects will be put into operation in 2012-2014. We believe that there will be several investment projects amounted more than 1.5mn sqm to be launched, and rental revenue in coming three years will keep stable growth.

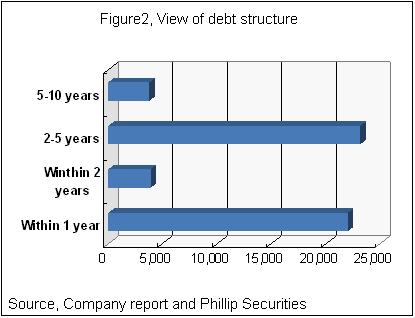

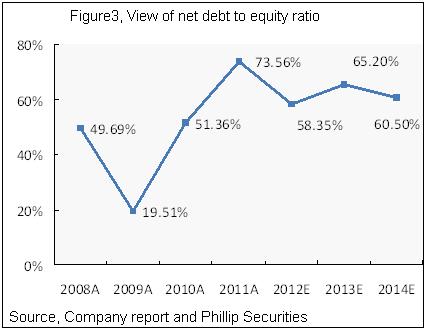

Debt of CRL rose obviously. Its debt at the end of 2011 soared by HKD 23.3bn to 48.8bn, and net debt to equity ratio climbed by 22.2 points to 73.6% with historical high level. In 2012 there will be 36% of total debt to be due, the company will renew and repay the short-term debt of 21.9bn, in our opinion. Therefore, we expect that CRL's net debt will drop with declining net debt to equity ratio of below 58% level in 2012. And the ratio in 2013 will maintain over 60% for large expense plan on investment properties.

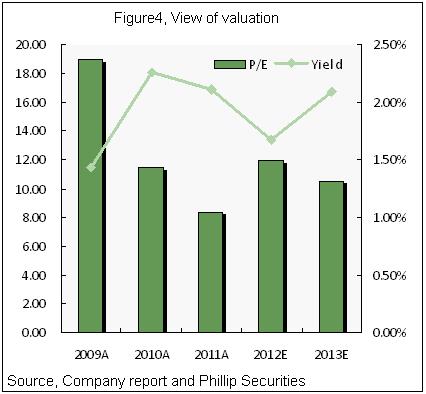

In our opinion, fundamental factors kept improving from 2011. Besides of over-forecasted sales performance, revenue from investment properties may ensure its keeping stable growth, which can make CRL enjoy higher valuation. Since Oct, 2011, the company's share price has dropped by 126%, and current price basically represented 10.5 times of forecasted P/E in 2013. We give CRL “Neutral” rating, 12m TP at HKD 16.2.

Sales rose significantly because of recovering market

Contracted sales of CRL in 1H2012 increased sharply, exceeding market forecast. Its contracted sales in the first six months reached RMB 20.6bn, significantly rising by 56% than 13.2bn in 1H 2011, and accounted for 52% of full-year sales target of 40bn. CRL's completion rate was obviously better than peers average because the company launched more positive selling strategy and house market had been recovering. Its sales in May and June reached 5bn and 4.3bn with obvious improvement.

Sales completion rate in the first three quarters will exceed 85%

We expect that the company will launch strong marketing plan in 3Q to complete the sales target of 40bn in advance. The company will launch new supplies of over 20bn in 3Q, and sales in 3Q will be 13.5bn with completion rate of more than 50%. Therefore, sales completion rate in the first three quarters will exceed 85%.

Revenue from investment properties kept increased

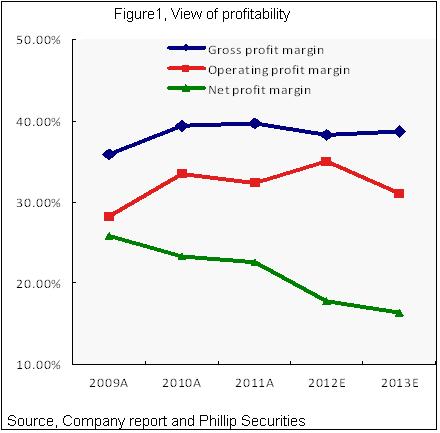

In 2011 CRL achieved revenue of HKD 35.8bn, rising by 39.1% YoY, in which revenue from investment properties reached HKD 2.79bn, rising by 57.1% YoY.

“The MIXc” and “Rainbow City”, two major brands of commercial properties, orient different market consumers respectively. Since 2011 the company accelerated its steps on commercial properties, and several projects have been opened one by one. Because more capital was put into investment properties, more projects will be put into operation in 2012-2014. We believe that there will be several investment projects amounted more than 1.5mn sqm to be launched, and rental revenue in coming three years will keep stable growth.

Net debt to equity ratio at the end of 2012 will decline

Debt of CRL rose obviously. Its debt at the end of 2011 soared by HKD 23.3bn to 48.8bn, and net debt to equity ratio climbed by 22.2 points to 73.6% with historical high level. In 2012 there will be 36% of total debt to be due, the company will renew and repay the short-term debt of 21.9bn, in our opinion. Therefore, we expect that CRL's net debt will drop with declining net debt to equity ratio of below 58% level in 2012. And the ratio in 2013 will maintain over 60% for large expense plan on investment properties.

Earning forecast

According to our estimation, CRL's booked revenue in 2012-2013 will increase stably, and revenue from investment properties will rise more rapidly. Total revenue in 2012-2013 will be HKD 42.5bn and 52.6bn, EPS at HKD 1.296 and 1.475, and pay out ratio will maintain over 20%.

Risk

Sales may progress slowly with dropping sales completion rate.

Short-term debt may not renew and repay smoothly.

Expense from investment properties will exceed forecast.

Valuation

In our opinion, fundamental factors kept improving from 2011. Besides of over-forecasted sales performance, revenue from investment properties may ensure its keeping stable growth, which can make CRL enjoy higher valuation. Since Oct, 2011, the company's share price has dropped by 126%, and current price basically represented 10.5 times of forecasted P/E in 2013. We give CRL “Neutral” rating, 12m TP at HKD 16.2.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()