-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

BYD (1211.HK) - Hit New High!

Thursday, July 14, 2022  2018

2018

BYD(1211)

| Recommendation | BUY |

| Price on Recommendation Date | $325.000 |

| Target Price | $399.000 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Sales Volume Soars by 163% YoY in June

The latest sales data show that BYD's new energy vehicle sales hit another record high in June: a total of 134,036 new energy vehicles were sold, up163% yoy and 17% mom, which is expected to be higher than the overall rise in domestic new energy vehicles. The cumulative sales volume for the first six months was 641,350 units, up 314.9% yoy, reaching 43% of the annual sales target of 1,500thousand units.

From the perspective of different types, the sales volume of new energy commercial vehicles was 274 units in June, down 78% yoy and 64% mom. The sales volume of pure electric passenger vehicles was 69,544 units, up 247% yoy and 30% mom, while the sales volume of plug-in hybrid electric vehicles was 64,218 units, up 219.5% yoy and 5.6% mom. The cumulative sales volume for the first six months was 323,519 and 314,638 units, respectively, up 246% yoy and 454% yoy. The former was mainly driven by the expansion of production at the Shenzhen plant, while the latter's slightly lower yoy growth was due to the impact of the shutdown of the Changsha plant for investigation..

A Number of Models Continue to Be Sold Well, and New Vehicle Models Are Launched Intensively

The overall vehicle market picked up in June as the resumption of work and production continued. With strong product competitiveness, the flagship model of the Dynasty series, Han, saw hot sales, recording sharp increases for several months in a row. In June, its sales volume exceeded 20 thousand units for two consecutive months, reaching 25,439 units, up 203% yoy, of which the delivery of Han DMI was up 386% yoy and that of Han EV closed to 13 thousand units. The cumulative sales volume for the first six months exceeded 250 thousand units, continuing to lead the sedan segment of the same class.

The sales of other models of the Dynasty series was also high: 8,134/26,623/32,077/19,731 units of the Tang/Qin/Song/Yuan series were sold in June, up 159%/71.7%/113%/1494% yoy, with a cumulative sales volume of 55,825/146,737/163,356/78,662 units in the first six months.

In addition, the Destroyer 05/Dolphin/e series recorded a sales of 7,464/10,376/3,918 units, respectively.

This year and next are major product years for BYD, which is expected to launch no less than 20 new vehicle models in total, including facelifts. This year, the Destroyer 05, Seal, Denza D9, 22 Tang EVs, 22 Han EVs, DM-i, DM-p and Qin Plus DM-i have already been launched, and in the second half of the year and next year, BYD will continue to launch Denza SUVs, the Warship series, Sea Lion and Seagull. The product matrix will be further improved and, judging from the current optimistic pre-sale situation, the product unit price is expected to continue to see upward breakthrough.

Continuous Capacity Release with Firm Policy Support

Since May, the Chinese government has announced a new round of new energy vehicles to the countryside, and the meeting of the State Council held in June explicitly supported the consumption of new energy vehicles and considered extending the preferential policy of exemption from the purchase tax on new energy vehicles, involving a total of 69 models from 26 vehicle companies, further expanding the coverage compared to 2021 (52 models from 18 brands in 2021). The local government has granted more subsidies to new energy vehicles compared to traditional fuel vehicles, reflecting the government's firm determination to the countercyclical adjustment and its resolute support for the development of the new energy vehicle industry. The renovation of the new plant in Changzhou and the Shenzhen plant and the second phase of the Changsha plant and the new plant in Hefei are expected to further release production capacity, which, coupled with the Company's long-term control of the supply chain, will provide strong support for the achievement of the annual sales target and may even beat expectations.

Investment Thesis

Therefore, although there are various challenges in the future, we believe that the Company is entering into a growth period with more stability and sustainability.

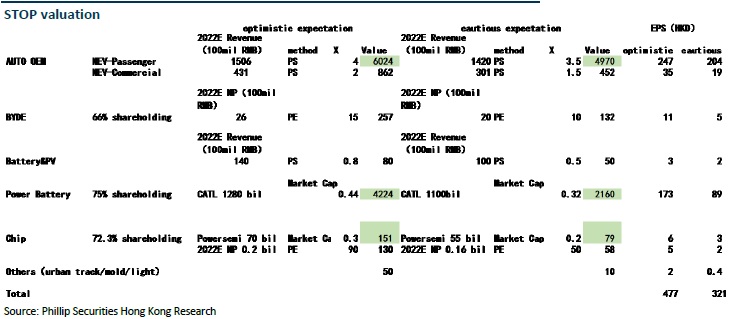

In terms of STOP valuation adopt, we give the original business (automobile, mobile phone, rechargeable battery and photovoltaic business) 296/230 HK$/per share, power battery business and semiconductor business from two assumptions of optimistic expectation and cautious expectation, and 173/89 and 5.5/2.5 HK$/per share, the overall valuation is respectively 477/321 HK$/per share, implying 47% and -1% upside respectively. For comprehensive consideration, we given the target price of 399 HK$, corresponding to 2022/2023/2024 127.5/74/53x P/E, 9.6/8.5/7.4x P/B, BUY rating. (Closing price as at 7 July)

Risk

Sales of NEVs is not as good as expected

New business risk

Slow-down of Hand-set components business

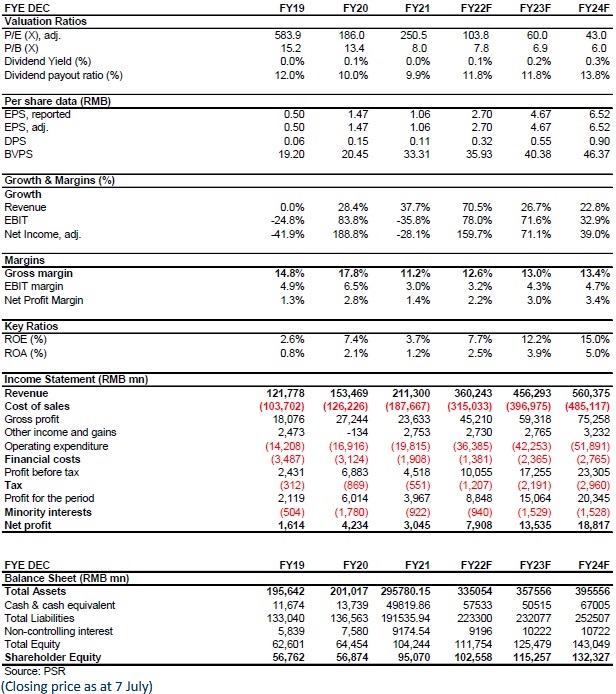

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()