-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Tianneng (819.HK) - The Recycling business is expected to become a new profit growth point

Wednesday, June 27, 2018  11473

11473

Tianneng(819)

| Recommendation | BUY |

| Price on Recommendation Date | $12.180 |

| Target Price | $14.700 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

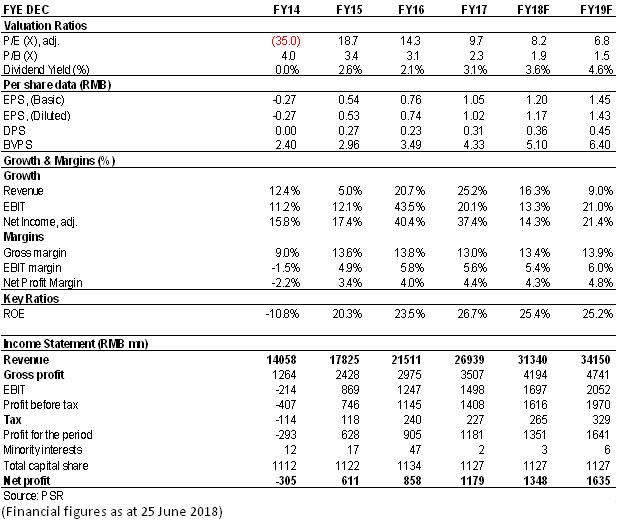

Tianneng Power is a leading enterprise in China's lead-acid power battery industry. We believe that the Company's lead-acid battery business will continue to maintain its stable growth characteristics and become the Company's ※cash cow§ business. Its recycle business revenue CAGR growth in future is expected to reach 50%. The company is the leader in the field of lead-acid batteries and has a sound financial position. Its new business forward plan is clear and pragmatic. We believe that a certain valuation premium should be given. We expect the company's EPS for 2018/2019 to reach 1.196/1.451 yuan and the target price of HK$14.7, corresponding to 2018/2019 10/8.2x P/E. (Closing price as at 25 June 2018)

Company Profile

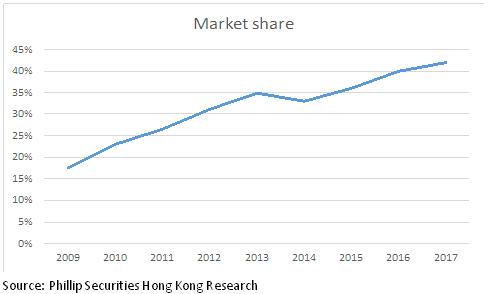

Tianneng Power is a leading enterprise in China's lead-acid power battery industry. Founded in 1986, the Company entered the lead-acid power battery field for electric bicycles and launched the “Tianneng” brand in 1998. In 2004, it began to engage in the R&D and production of lithium batteries. After over three decades of development, the Company has become a new energy high-tech enterprise that integrates electric vehicle power battery, wind energy solar energy storage battery, and battery recycling and other businesses, establishes its mature sales channel, and steadily increases its market share. Its market share of lead-acid battery industry is 42%, and the total market share of lead-acid power battery industry of the Company and Chaowei Battery exceeds 80%, forming an industry duopoly pattern.

The Company owns eight production bases in four provinces in China, which are located in (1) Changxing Headquarters, (2) Meishan and (3) Heping in Changxing County of Zhejiang Province, (4) Shuyang County of Jiangsu Province, (5) Wuhu City and (6) Jieshou City of Anhui Province, (7) Puyang City and (8) Jiyuan City of Henan Province, respectively. The Company now has 300 thousand terminal stores and 3000 dealers.

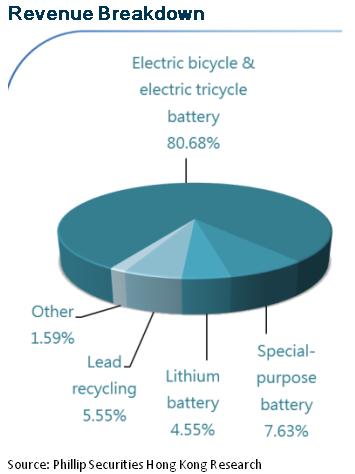

The Company's existing business is divided into five categories, namely 1) electric bicycle lead power battery, 2) special purpose lead power battery, 3) new energy lithium battery, 4) recycling of waste batteries, and 5) smart energy. In terms of revenue, the first two categories are the Company's traditional businesses, which account for about 89% of revenue. The latter three are emerging sectors, which represent a rapid growth although occupying a relatively smaller share.

Financial overview

Electric bicycles have been rapidly popularized in China due to their convenience, practicality, and economy. The output has grown rapidly from 300,000 electric bicycles in 2000 to 36.95 million electric bicycles in 2013. The compound annual growth rate was up to 50%. Afterwards, the output declines, but it still maintains at an annual yield of 30 million electric bicycles. Lead-acid batteries account for about 95% of the market share of electric bicycle power batteries.

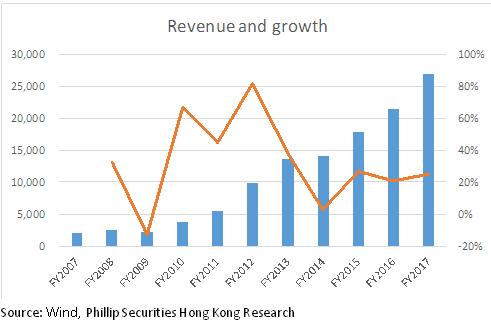

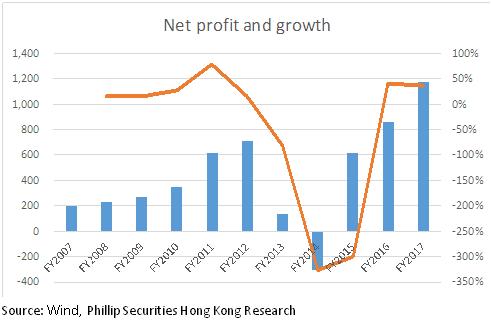

Benefited from high industrial growth, since the Company's listing in 2007, its operating revenue has reported a compound annual growth rate of 30%, and its net profit has reported a compound annual growth rate of 19.2%. There has been a decline in result only due to the government's efforts to strengthen environmental protection supervision and industry price war in 2013-2014. Due to fluctuations in lead prices and the price competition strategies of the Company, the Company's gross margin has gradually decreased from 20-30% a decade ago to 10-14%, but its market share has increased from 23% in 2010 to 42% currently.

In 2017, the Company's revenue reached RMB26.9 billion, up 25.2% yoy; the net profit attributable to shareholders was RMB1.178 billion, up 37.3% yoy; the diluted earnings per share were RMB1.02, and the final dividend per share was HKD0.37 with a payout ratio of 30%.The gross margin was approximately 13.04%, down 0.8% yoy, which was mainly because the price of lead (which is the main raw material for lead batteries) has increased and the utilization rate of lithium battery business was still climbing. However, the Company's expenses are properly controlled, and the operating expense ratio decreases by approximately 0.4 ppts to 4.75%. The net profit rate increases by 0.17 ppts to 4.38%, the ROE increases by 3.3 ppts to 26.75%, and the result is better than its peers.

The sales revenue of new energy lithium battery was approximately RMB1.223 billion, up 98.68% yoy; the sales revenue of special-purpose battery sales revenue was approximately RMB2.054 billion, up 5.10% yoy; the sales revenue of lead-acid power batteries for electric bicycles and electric tricycles was approximately RMB21.707 billion, up 26.83% yoy.

Lead-acid part will remain steady, with its "cash cow" nature is not changed

We believe that the Company's lead-acid battery business will continue to maintain its stable growth characteristics and become the Company's ※cash cow§ business, based on the following perspectives:

1) The economic development between China's urban and rural areas is extremely uneven. Electric bicycles/tricycles have a vast market in terms of travel and logistics. Even if the growth rate drops, there is still a huge replace demand market. The cost-effectiveness of lead-acid batteries is enough to protect its dominant position in the mid-to-short term. At present, the proportion of new market and replace market is about 2:8. One bicycle/tricycle needs 3-5 batteries while the battery life is about 1.5-2.5 years. According to Ipsos Business Consultancy Forecast, by 2025, the demand for electric tricycle batteries will reach RMB60 billion.

2) In recent years, the Chinese government has continued to increase its efforts to rectify environmental protection and increase supervision of the lead-acid battery industry. The price war has also led to the elimination of many small-scale lead-acid battery manufacturers. The industry concentration has continued to increase, and the possibility and necessity of price war have greatly reduced and it is expected that the battery price will maintain a relatively stable range.

3) The Company is actively developing new lead battery utilization markets, including four-wheel low-speed electric vehicles. The tubular batteries for electric forklifts, the starter batteries for conventional automobiles, and the energy storage battery systems for wind energy solar energy are newly added. Specifically, we believe that the market potential of mini low-speed electric car is huge, and still in rapid development. The large lead-acid batteries part is worth looking forward to.

The Recycling business is expected to become a new profit growth point

The Company previously announced that its business focus in the next 3-5 years will be tilted toward emerging businesses such as low-speed electric vehicle lead-acid batteries, new energy lithium batteries, and battery recycling. The 3Gwh power lithium battery and 15GVAh lead-acid power battery project invested by the Company have partly been put into use.

“Client first” will be the emphasis of the Company's lithium business. The Company's NEV customers include Chery, Conti, Lifan, FAW, Zhongtai, Niudian, Yadea, and shared e-bicycle companies ; Tianneng's lithium battery products have excellent performance and pipeline advantages. In the future, they will fully benefit from the increase in the penetration rate of lithium batteries. Among the mini low-speed car customers, Yujie, Shifeng, Tangjun and several other mainstream companies all use Tianneng's products.

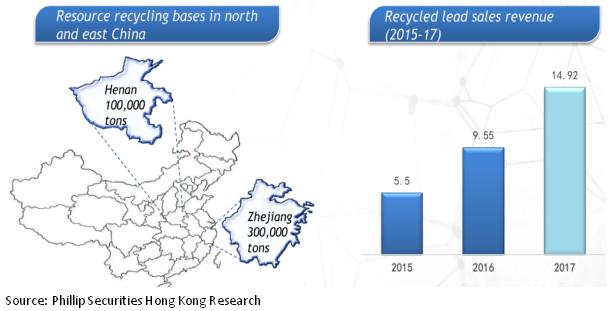

For recycle business, the Company has two major waste battery recovery bases in Zhejiang and Henan, with an annual processing capacity of 400,000 tons and a lead recovery rate of 99%. It is the largest harmless recycling waste battery company in China and can produce 25-28 million tons of recycled lead. Since the lead entry threshold for lead recycling industry is extremely stringent, with the growth of scrap-acid batteries, this business revenue CAGR growth in future is expected to reach 50%.

Investment Thesis

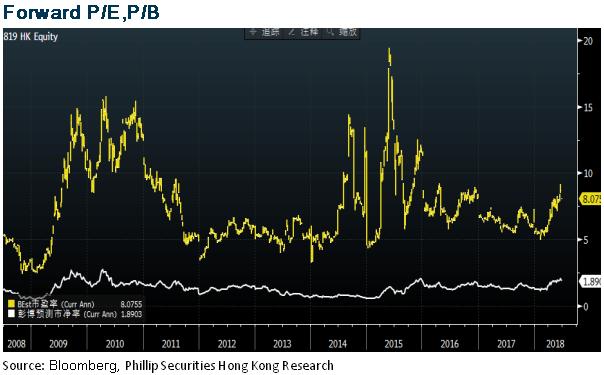

The Company's Balance sheet is strong, holding net cash as high as 3.27 billion, and the gearing ratio is only 16%. The company is the leader in the field of lead-acid batteries and has a sound financial position. Its new business forward plan is clear and pragmatic. We believe that a certain valuation premium should be given. We expect the company's EPS for 2018/2019 to reach 1.196/1.451 yuan and the target price of HK$14.7, corresponding to 2018/2019 10/8.2x P/E.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()