-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of January 2022

Monday, February 7, 2022  1559

1559

Report Review of January 2022

Weekly Special - 3306 JNBY Design Limited

Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

Automobile & Air (ZhangJing)

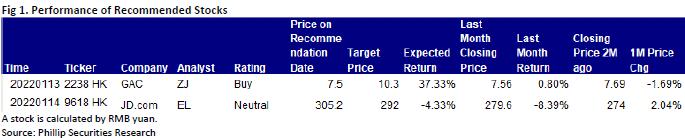

This month I released updated reports of GAC (2238.HK).

One of the characteristics of China`s auto market in 2021 is: the market share of Chinese brands is further increasing. In December 2021, the market share of Chinese brands in passenger vehicles was 45.7%, a year-on-year increase of 6.2 pts. In 2021, China The brand`s market share increased to 42.3%, an increase of 6.4 pts over the whole year of 2020. The reason is that after years of intense market competition, many Chinese brands have continuously improved their competitiveness, and finally stood out under the trend of the new four modernizations of automobiles. Among them, the popularization of new energy vehicles has contributed greatly. In 2021, new energy vehicles drove the market share of Chinese brands to increase by 6.2%, and the driving force increased by 3.8 pts year-on-year. In terms of ASP, benefiting from consumption upgrades and the continuous introduction of new models and new brands, the sales of Chinese brand passenger vehicles in 2021 will be below RMB 100,000, 100,000-200,000, 200,000-300,000, and above 300,000. The proportions within the range are 48.9%, 42.1%, 5.9% and 3.0%, respectively -6.8/+2.4/+3.2/+1.3 pts compared with the whole year of 2020. The trend of upgrade is obvious. We suggest to pay attention to GAC Group, whose brand has an obvious upward trend.

According to the latest sales data, since the fourth quarter, the sales volume of major automotive joint ventures has climbed month by month, reflecting that the chip shortage dilemma has been eased month by month. In Oct/Nov/Dec, GAC Honda sold 75.4/77.7/78.4 thousand units, +4.7%/+3.04%/+0.9% mom and -13.94%/-9.97%/-3.5% yoy respectively; As for GAC Toyota, it sold 61/85/99 thousand units, +26.29%/+39.34%/+15.9% mom and -15.3%/+9.82%/36.5% yoy. There was an obvious trend of recovery. Key models, such as Accord, Vezel, Levin, and Highlander, recorded good sales volume. Automotive joint ventures are starting a strong product cycle and speeding up the layout of new energy vehicles. The profitability is expected to rebound with the successive launch of new models, such as GAC Honda`s Integra and e:NP1, and GAC Toyota`s Sienna, Fenglanda, Venza, and bZ4X.

In terms of self-owned brands, GAC`s self-owned brands sold 47/50.6/32.2 thousand units in Oct/Nov/Dec, +29.8%/+6.8%/-9.6% mom and +25.4%/+24.7%/+2.2% yoy. Specifically, the sales volume of Trumpchi Empow has exceeded 10 thousand units for two consecutive months. GAC Aion, a new energy vehicle brand, had strong terminal demand. Its shipments were second only to that of Tesla and BYD, and the sales volume has exceeded 10 thousand units for seven consecutive months. The new second-generation GS8 equipped with THS was launched in December. Aion LX Plus, which has a super miles range of over 1,000 km, is expected to be launched early 2022. In 2022, GAC Aion will have a new production capacity of 100 thousand units per year. The proportion of new energy vehicles is expected to be further increased. Recently, the asset reorganization and capital increase plan of GAC Aion has been determined, which will accelerate the launch process. In the future, GAC Aion`s net assets will exceed RMB10 billion, and it will have complete R&D capabilities of new energy pure electrically-powered vehicles, independent production plant and its own pipelines. The accumulation of funds and technology and the improvement of efficiency will help GAC Aion store energy for the development of new energy vehicles.

We expect that under the trend of accelerating the electric and intelligent layout, the Company`s joint venture brands with Japanese companies will continue to expand their advantages. Self-owned brands are also expected to open up room for growth.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released an updated report of JD.com, Inc. (09618.HK).

JD.com, Inc. (JD) operates online retail and marketplace e-commerce businesses, as well as fulfillment services. For the online retail business, JD sells self-operated products and thirdparty merchant products through its own online e-commerce platform, and provides digital marketing services to online retail business suppliers, third-party merchants and other partners. JD also collaborate with Walmart on e-commerce by launching Walmart and Sam`s Club Flagship Stores on its platform and providing fulfillment solutions to them. Through strategic partnership with Dada Group, JD Logistics to provide customers with on-demand and last-mile delivery services of a wide selection of grocery and other fresh products through JD-Daojia. JD also explores in the offline retail market through 7FRESH, an offline fresh food markets, experimenting on the omni-channel model.

In 3Q21, the revenue was RMB218.7bn, an increase of 25.5% YoY. Despite of weak consumption and tight supply chain, JD`s growth rate still exceeded the guidance given previously by the management. The net product revenue during the period was RMB 186 billion, an increase of 22.9% YoY; net service revenue was RMB32.7bn, an increase of 43.3% over the same period in 2020. The overall gross profit margin decreased by 1.2ppt YoY to 14.2%, mainly because operating costs increased by 27.3% from RMB147.4bn in the 3Q21 to RMB187.6bn in the 3Q21. Net loss attributable to shareholders in the 3Q was RMB2.8bn (compared to net profit of RMB7.6 billion in the same period last year). However, the non-GAAP net profit attributable to shareholders was RMB5bn, down 9.2% from RMB5.6bn in the same period 2020, and still better than market consensus.

In Q3, GMV of JD`s omni-channel business grew by nearly 100% YoY. Through further analysis of online and offline comprehensive data, JD would continue to provide differentiated products that best suit the needs of potential customers of various offline franchise stores, and provide customers with a more dynamic and interactive integrated omni-channel shopping experience.

Non-GAAP NPM was 2.3%, down 0.9ppt from 3Q20, still above market consensus. 4Q21 revenue growth momentum would continue, as double 11 transaction volume in 2021 reached RMB349.1bn, an increase of 28.6% compared with 2020 record of RMB271.5bn.

The competition with other e-commerce platforms such as Alibaba (09988) has intensified. However, based on the fact that JD`s 3Q21 performance exceeded the previous guidance given, the management also expects that revenue growth would sustain into 4Q21. Therefore, we expect JD`s full-year revenue to grow 29% YoY in 2021, which is similar to the first three quarters in 2020. Tencent (00700) recently announced that it will distribute most of its holdings of JD (more than 100bn JD shares, its stake will drop from 16.9% to 2.3%) as special interim dividend to Tencent`s shareholders. It is expected that Tencent`s decision (distributing JD shares in late March) will cause JD`s share price to suffer technically in the next few months. Thus, JD`s share price has l geared more toward the downside rather than outperform the market, but we believe there will be no structural damage to JD`s long-term fundamentals.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()