-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

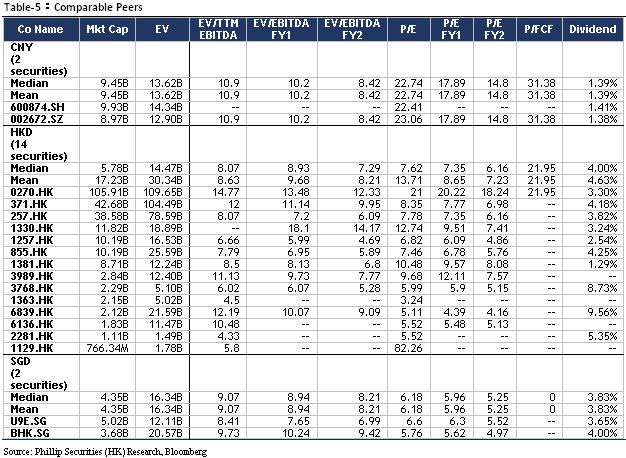

BJ ENT WATER (371.HK) - Results of 1H2019 in Line, Asset-Light Transformation is Expected

Wednesday, September 11, 2019  6244

6244

BJ ENT WATER(371)

| Recommendation | BUY |

| Price on Recommendation Date | $4.260 |

| Target Price | $5.830 |

Weekly Special - 3306 JNBY Design Limited

Company Update

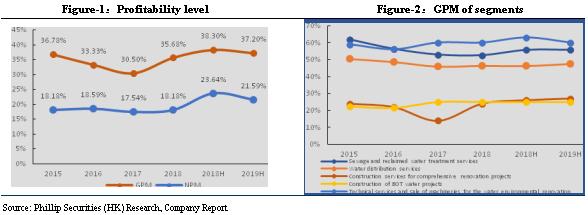

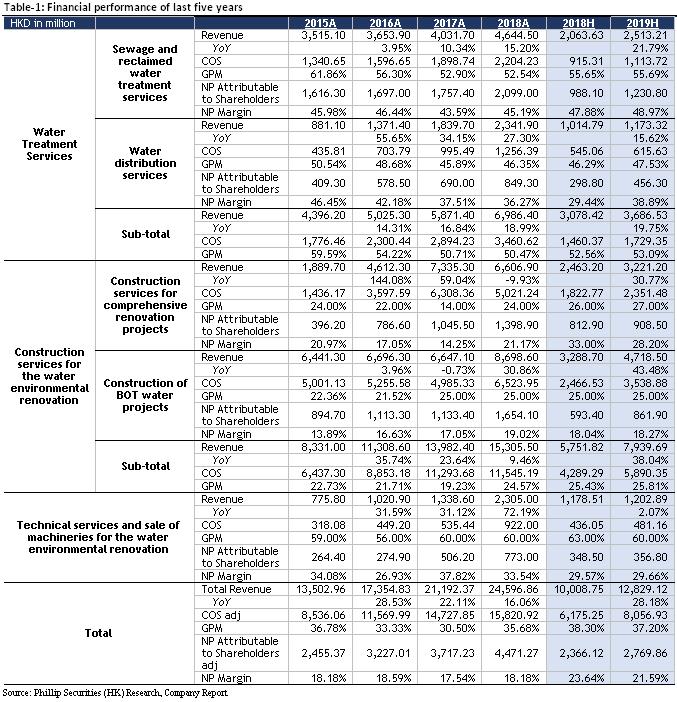

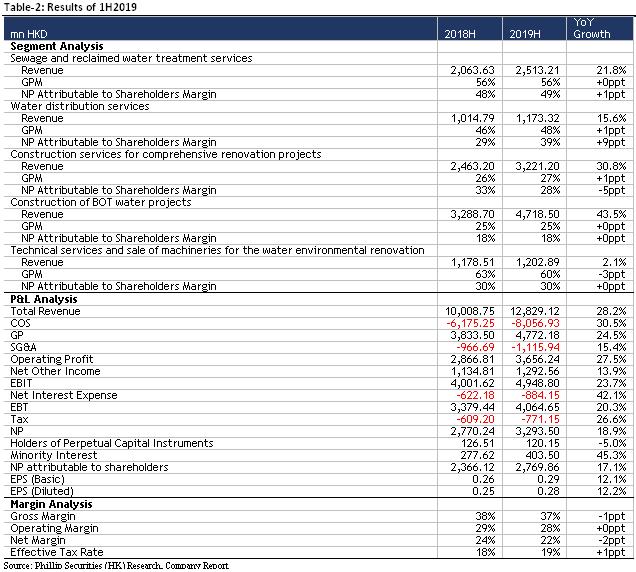

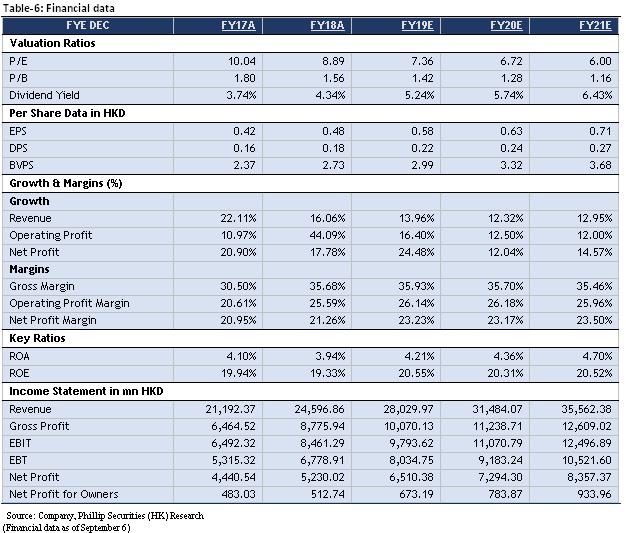

For the six months ended 30 June 2019, the company's revenue was HKD 12.829 billion (corresponding period in 2018: HKD 10.009 billion), representing an increase of 28.18%. Revenue from Sewage and reclaimed water treatment services was HKD 2.513 billion (corresponding period in 2018: HKD 2.064 billion), representing an increase of 21.79%. Revenue from Water distribution services was HKD 1.173 billion (corresponding period in 2018: HKD 1.015 billion), representing an increase of 15.62%. Revenue from Construction services was HKD 7.94 billion (corresponding period in 2018: HKD 5.752 billion), representing an increase of 38.04%. Revenue from Construction services for comprehensive renovation projects was HKD 3.221 billion (corresponding period in 2018: HKD 2.463 billion), representing an increase of 30.77%. Revenue from Construction of BOT water projects for comprehensive renovation projects was HKD 4.719 billion (corresponding period in 2018: HKD 3.298 billion), representing an increase of 43.48%. Revenue from Technical services and sale of machineries for the water environmental renovation for comprehensive renovation projects was HKD 1.203 billion (corresponding period in 2018: HKD 1.179 billion), representing an increase of 2.07%. The gross profit was HKD 4.771 billion (corresponding period in 2018: HKD 3.834 billion), representing an increase of 24.49%. The GP margin was 37.10%, decreasing by 1.1 ppt compared with 1H2018, which is mainly due to the change of revenue portfolios. Profit attributable to equity holders of the company was HKD 2.77 billion (corresponding period in 2018: HKD 2.366 billion), representing an increase of 17.06%. Basic and diluted earnings per share were HK28.68 cents and 28.25 cents respectively. The interim dividend of HK10.7 cents per ordinary share for the six months ended 30 June 2019 (six months ended 30 June 2018: HK9.5 cents per ordinary share), showing an increase of 12.63%, the payout ratio is 37%, same as 1H2018.

The company's performance of core business is basically consistent with our forecast, related performance increase in total revenue was mainly contributed from the increase of water treatment services and construction services for the water environmental renovation. Total daily design capacity for new projects secured for the period was 1,355,925 ton, the net increase in total daily design capacity of the period was 936,925 tons, less than the company's guidance of 4 million tons additional for the full 2019. But the company maintain the above new capacity target, believing there will be more opportunities of M&A in 2H2019.

Stable growth in production capacity, waiting for high quality M&A opportunities

As at 30 June 2019, the company entered into service concession arrangements and entrustment agreements for a total of 1,047 water plants including 875 sewage treatment plants, 140 water distribution plants, 30 reclaimed water treatment plants and 2 seawater desalination plants. Total daily design capacity for new projects secured for the period was 1,355,925 tons including BOT projects of 130,000 tons, PPP projects of 882,925 tons, entrustment operation projects of 263,000 tons, and 80,000 tons through mergers and acquisitions. Due to different reasons such as expiration of projects, the company exited projects with aggregate daily design capacity of 419,000 tons during the period. As such, the net increase in daily design capacity of the period was 936,925 tons. As at 30 June 2019, total daily design capacity was 37,761,558 tons. The company's production capacity has maintained a compound annual growth of 35.96% since 2008. Although the progress of new projects in 1H2019 has slowed down, we are still optimistic about the company's capacity growth in 2H2019. We expect that the company will achieve the goal of adding 4 million tons of new capacity in 2019 through more M&A projects.

Continue asset-light transformation, closely cooperate with the Three Gorges Group

On January 18, 2019, the company entered into a subscription agreement with China Yangtze Power International, which has conditionally agreed to subscribe for 470,649,436 new ordinary shares. This means that the company will further deepen its partnership with China Three Gorges Corporation, to develop water environmental protection business in the Yangtze River area. In addition, the company also adheres to the “dual-platform strategy” and asset-light business model. It is expected that there will be a new signed RMB 20 billion water environment renovation projects and a capital expenditure of HKD 12 billion for the whole year. The interest expense for 1H2019 has also increased 42.73% to HKD 1.193 billion, the gearing ratio dropped from 114% to 110%. However, we expect that as the company's asset-light model continues to promote, the future capital expenditure will gradually decline, and the financial situation will further improve.

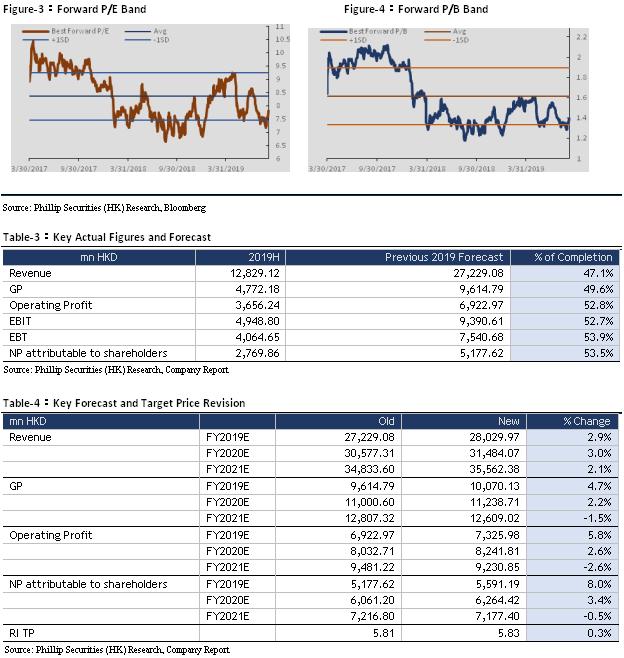

Financial Forecast and Valuation

We adjust the company's revenue in FY19/FY20/FY21 to be HKD 28.0/31.5/35.6 billion, representing increases of 13.96%/12.32%/12.95% YoY; net profit attributable to shareholders will be HKD 5.6/6.3/7.2 billion, representing increases of 25.05%/12.04%/14.57% YoY; corresponding EPSs are HKD 0.58/0.63/0.71. We adjust the TP of HKD 5.83, corresponding to FY19/FY20/FY21 10.06x/9.19x/8.21x PE with a +36.76% potential upside compared with CP of HKD 4.26 as of September 6, 2019, we maintain “BUY” investment rating.

Risk

1. Project progress fail expectations; 2. Industry policy; 3. Interest rate; 4. M&A fails expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()