-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Jumpcan Pharma (600566.SH) - Pudilan Entered into Shandong PDRL; Robust FY17&18Q1 Results

Wednesday, April 25, 2018  12805

12805

Jumpcan Pharma(600566)

| Recommendation | Accumulate |

| Price on Recommendation Date | $47.860 |

| Target Price | $51.600 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

We highlight that: 1) PAOL and SGYX pill entered into Shandong PDRL; 2) Strong growth in FY17 & 18Q1; 3) Intensifying sales network; 4) Issuing convertible bonds to fund capacity expansion; 5) R&D going well. We assume topline growth in 18E/19E to be 30%/25% and target PE 30x conservatively, thus we get target price of RMB51.6, Accumulate recommendation. (Closing price at 23 Apr 2018)

Business Overview

Pudilan and SGYX pill entered into Shandong PDRL. The company announced on 29 Mar that its exclusive formula Pudilan Anti-inflammatory Oral Liquid (PAOL) and ShenGuiYangXue pills entered into Shandong PDRL, Class II (乙类). We expect the sales volume to hike after implementation of PDRL.

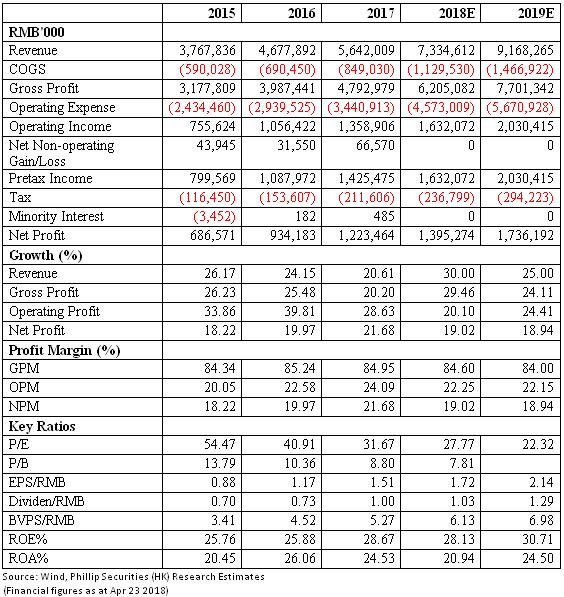

Strong FY17 & 18Q1 Results. We see stable growth in 2017: the company achieved revenue of RMB5.64bn (+20.6% YoY), net profit attributable to shareholders of RMB1.22bn (+30.97% YoY) and net profit excluding non-recurring items of RMB1.15bn (+28% YoY). Manufacturing segment turnover reached RMB5.43bn and distribution segment turnover amounted to RMB0.21bn. Selling expenses reported 17.3% YoY growth, roughly in line with topline growth. R&D expenses rose by 34.5% YoY to RMB195mn mainly due to increasing investment in R&D. We also highlight notable growth in 18Q1, which is beyond market expectations: 18Q1 topline was up by 51.45% YoY to RMB2.13bn. GPM remained relatively stable around 84.7% and selling expenses increased by 45%, which generally synchronized with sales growth.

Issuing Convertible Bond to Expand Capacity. In 18Q1, financing costs rose dramatically to RMB3.35mn, attributable to new issuance of RMB828mn convertible bond, which is mainly used to fund capacity expansion (involving the establishment of new buildings, liquid factories, etc.).

Intensifying Distribution Network. The company focuses on three segments, namely Western & Traditional Chinese medicines, TCM daily chemical articles and TCM healthcare products. It continues to enhance distribution channels including hospitals, OTC stores, clinics and supermarkets. With implementation of policies involving tiered medical services and medical union, the company entered more blank regions through intensive academic promotion in primary hospitals. For OTC channel, the company built a strong OTC sales team and enhanced cooperation with other OTC platforms. We see that sales of Iron Proteinsuccinylate Oral Solution (IPOS) and products of newly-acquired subsidiary Dongke continue to climb in 2017.

Progress of Pipeline. During 2017, the company gained production approval of Yangyingqingwei Granules (YYG), clinic trail permissions of three products and six patents. It also launched the construction of Shanghai research center. R&D progress is going well.

Investment Thesis & Valuation

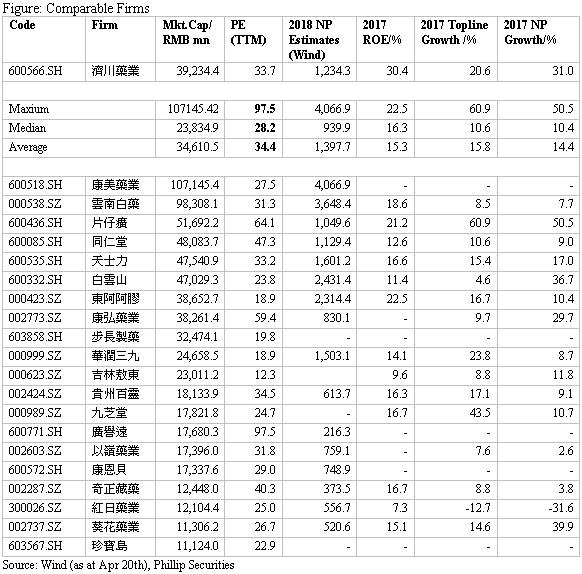

We increase target price to RMB51.6. Given continuously rising sales volume of main products, we estimate that revenue growth to be 30%/25% and EPS to be RMB1.72/2.14 in 18E/19E, with relatively stable margins. We see that currently the average PE of TCM sector is around 28.2x-34.4x. We conservatively assume target PE ratio of 30x to derive 2018 target price of RMB51.6, Accumulate recommendation. (Closing price at 23 Apr 2018)

Risks

Slow than expected expansion of distribution network;

Policy risks;

R&D failure.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()