-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Tencent Holdings (700.HK) - Optimistic ``Internet +`` Strategic Outlook

Wednesday, March 23, 2016  9316

9316

Tencent Holdings(700)

| Recommendation | Accumulate |

| Price on Recommendation Date | $158.100 |

| Target Price | $182.000 |

Weekly Special - 3306 JNBY Design Limited

2015 Results Continued to Grow Rapidly

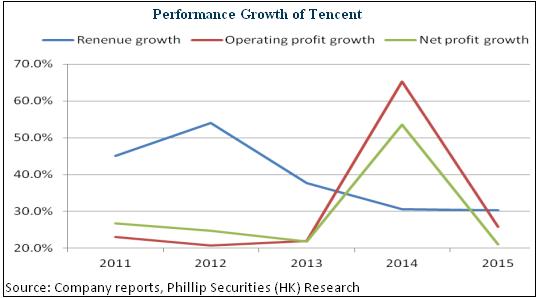

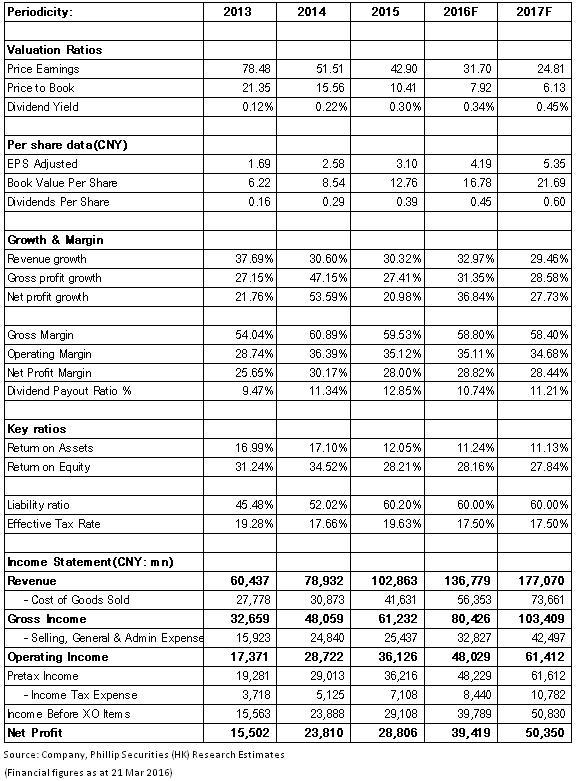

The total revenue and net profit of Tencent Holdings in 2015 stood at RMB102.9 billion and RMB28.8 billion, a YoY increase of 30% and 21% respectively. Besides, its EPS amounted to RMB3.1, and its net operating cash flow soared by 32% to RMB45.4 billion. Overall, it maintained the rapid growth in 2015.

The revenue growth was mainly attributed to the increase in smart device MAU of QQ and MAU of WeChat, rising by 11% to 697 million and by 39% and to 642 million respectively over the same period last year. Such rise fueled the surge in online ads revenue by 110% to RMB17.5 billion, of which performance advertising and brand advertising jumped by 172% and 72% respectively. Additionally, the contribution proportion of the mobile platform to the revenues was up to 65%, and its proportion exceeded 85% in the fourth quarter. Meanwhile, thanks to the Company`s powerful concession operations of computer games and the huge mobile traffic, its online game business saw an increase of 26% and its social network revenues witnessed a growth of 30%, maintaining a steady growth.

In respect of profitability, although the gross profit margin fell by 1.4 percentage points to 59.5% year on year, the main reason for the fall is that the gross profit margin included the commissions to third-party game and content providers. The relatively low net profit growth was primarily because the Company`s financial costs grew by 37% due to increased loans and because the income tax expense also shot up by 39%. Furthermore, provision for impairment of the Company`s listed associate corporations engaging in e-business led its share of losses from the associate corporations increase RMB2.45 billion as compared with the same period last year, which also produced a significant negative impact on the results. But this is a non-recurring factor.

WeChat Supported Mobile Advertising Business Development

Large as the customer base of WeChat was, yet, as of September 2015, the penetration rate of WeChat was 69%, 43%, 27% and 28% in the second-tier to the fifth-tier cities respectively, far lower than the penetration rate of over 90% in the first-tier cities. Therefore, WeChat still has potential for development in the second-tier to the fifth-tier cities. Presently, WeChat has already found its way in all aspects of the users` life including socializing, reading, shopping and sports, so its dividends will continue to be released and thus the mobile advertising business is expected to become the engine of growth.

Additionally, by virtue of WeChat Payment and more diverse payment scenarios, the Company`s online payment business is booming, the users who have integrated bank cards with WeChat Payment has rapidly increased to 300 million, the vast majority of whom are active users. According to estimates, the monthly transfer transaction amount between users of WeChat has exceeded RMB100 billion, so the Company`s future prospects for Internet financial services are worth looking forward to.

Optimistic "Internet +" Strategic Outlook

Tencent actively promotes the "Internet +" strategy, with the vision of becoming China`s all-rounded service Internet provider featured by "Connect Everything." We believe the Company boasts immense amounts of users` data and traffic, gets a comprehensive understanding of consumer demand through big data resources, and by expanding products and services, invests in a wide range of vertical areas and enriches application scenarios, so its outlook for the "Internet +" ecosystem construction is optimistic.

Specifically, the Company`s game business will keep a leading position by its platform position and leading VR layout. Moreover, its online ads business will maintain rapid growth thanks to enhanced user participation by more video inputs and online payment. We grant the Company the target price of HK$182, equivalent to 36.5x EPS in 2016, with the "Accumulate" rating. (Closing price as at 21 Mar 2016)

Risk

The terminal game business declines more than expected;

Headway in mobile advertising service falls short of expectation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()